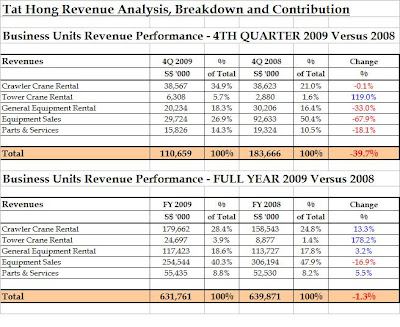

From the above diagram and breakdown, it can be seen that for 4Q 2009, crane rental took up a more significant portion of revenues at 40.6% (combining crawler and tower crane rentals), compared to just 22.6% a year ago. Granted, this was based on a lower revenue base (total revenue dipped from S$183.7 million to S$110.7 million for 4Q 2009 against 4Q 2008, a 40% drop) but it illustrates how Tat Hong are slowly but surely moving towards a “rental” business model, and how it can help to sustain revenues and cash flows.

If we dig deeper, it can be seen that crawler crane rental revenues barely dipped for 4Q 2009 compared to a year ago, with revenues holding steady at S$38.6 million. By contrast, sale of cranes fell 68% as the global downturn sucked up financing for companies and left them high and dry and unable to commit to more capex, hence hurting this division severely. Revenues from sale of cranes for 4Q 2009 fell from S$92.6 million to just S$29.7 million, and from the looks of things, is likely to worsen even further for 1Q 2010. Tower cranes, on the other hand, show good growth prospects as they now occupy 5.7% of Tat Hong’s total revenue pie (for 4Q 2009) and saw a 119% year-on-year revenue growth. General Equipment rental suffered a decline due to the discontinuance of the waste management division and heavy haulage New South Wales Division.

As reported by the Company, the extended wet season in North Queensland in 4Q 2009 also affected sales. Interesting to note is that for the first time, the % contribution from equipment sales fell below that of crawler crane rental, registering 26.9% compared to 34.9%, which very clearly shows the shift from equipment sales (a low margin business division) to crane rental (a much higher margin business division). Read more...

Further Reading

Tat Hong – FY 2009 Financial Analysis and Review Part 1

From the above diagram and breakdown, it can be seen that for 4Q 2009, crane rental took up a more significant portion of revenues at 40.6% (combining crawler and tower crane rentals), compared to just 22.6% a year ago. Granted, this was based on a lower revenue base (total revenue dipped from S$183.7 million to S$110.7 million for 4Q 2009 against 4Q 2008, a 40% drop) but it illustrates how Tat Hong are slowly but surely moving towards a “rental” business model, and how it can help to sustain revenues and cash flows.

If we dig deeper, it can be seen that crawler crane rental revenues barely dipped for 4Q 2009 compared to a year ago, with revenues holding steady at S$38.6 million. By contrast, sale of cranes fell 68% as the global downturn sucked up financing for companies and left them high and dry and unable to commit to more capex, hence hurting this division severely. Revenues from sale of cranes for 4Q 2009 fell from S$92.6 million to just S$29.7 million, and from the looks of things, is likely to worsen even further for 1Q 2010. Tower cranes, on the other hand, show good growth prospects as they now occupy 5.7% of Tat Hong’s total revenue pie (for 4Q 2009) and saw a 119% year-on-year revenue growth. General Equipment rental suffered a decline due to the discontinuance of the waste management division and heavy haulage New South Wales Division.

As reported by the Company, the extended wet season in North Queensland in 4Q 2009 also affected sales. Interesting to note is that for the first time, the % contribution from equipment sales fell below that of crawler crane rental, registering 26.9% compared to 34.9%, which very clearly shows the shift from equipment sales (a low margin business division) to crane rental (a much higher margin business division). Read more...

Further Reading

Tat Hong – FY 2009 Financial Analysis and Review Part 1For Part 2 of my analysis for Tat Hong’s results, I will be focusing on their business divisions and analysing the performance of each, as well as highlighting the sales mix which has changed from FY 2008 to FY 2009. It is hoped that through this analysis, it will be possible to pinpoint whether Tat Hong is able to continue to maintain their gross margins and also whether they can sustain themselves with cash until the downturn has eased. Pump-priming measures introduced by the various Governments will be discussed in Part 3, including prospects for each division and how Tat Hong will change its focus gradually over the next few years as their China division grows stronger.

Business Unit Revenue Contribution, Sales Mix and Performance Review

From the above diagram and breakdown, it can be seen that for 4Q 2009, crane rental took up a more significant portion of revenues at 40.6% (combining crawler and tower crane rentals), compared to just 22.6% a year ago. Granted, this was based on a lower revenue base (total revenue dipped from S$183.7 million to S$110.7 million for 4Q 2009 against 4Q 2008, a 40% drop) but it illustrates how Tat Hong are slowly but surely moving towards a “rental” business model, and how it can help to sustain revenues and cash flows.

If we dig deeper, it can be seen that crawler crane rental revenues barely dipped for 4Q 2009 compared to a year ago, with revenues holding steady at S$38.6 million. By contrast, sale of cranes fell 68% as the global downturn sucked up financing for companies and left them high and dry and unable to commit to more capex, hence hurting this division severely. Revenues from sale of cranes for 4Q 2009 fell from S$92.6 million to just S$29.7 million, and from the looks of things, is likely to worsen even further for 1Q 2010. Tower cranes, on the other hand, show good growth prospects as they now occupy 5.7% of Tat Hong’s total revenue pie (for 4Q 2009) and saw a 119% year-on-year revenue growth. General Equipment rental suffered a decline due to the discontinuance of the waste management division and heavy haulage New South Wales Division.

As reported by the Company, the extended wet season in North Queensland in 4Q 2009 also affected sales. Interesting to note is that for the first time, the % contribution from equipment sales fell below that of crawler crane rental, registering 26.9% compared to 34.9%, which very clearly shows the shift from equipment sales (a low margin business division) to crane rental (a much higher margin business division). Read more...

Further Reading

Tat Hong – FY 2009 Financial Analysis and Review Part 1

From the above diagram and breakdown, it can be seen that for 4Q 2009, crane rental took up a more significant portion of revenues at 40.6% (combining crawler and tower crane rentals), compared to just 22.6% a year ago. Granted, this was based on a lower revenue base (total revenue dipped from S$183.7 million to S$110.7 million for 4Q 2009 against 4Q 2008, a 40% drop) but it illustrates how Tat Hong are slowly but surely moving towards a “rental” business model, and how it can help to sustain revenues and cash flows.

If we dig deeper, it can be seen that crawler crane rental revenues barely dipped for 4Q 2009 compared to a year ago, with revenues holding steady at S$38.6 million. By contrast, sale of cranes fell 68% as the global downturn sucked up financing for companies and left them high and dry and unable to commit to more capex, hence hurting this division severely. Revenues from sale of cranes for 4Q 2009 fell from S$92.6 million to just S$29.7 million, and from the looks of things, is likely to worsen even further for 1Q 2010. Tower cranes, on the other hand, show good growth prospects as they now occupy 5.7% of Tat Hong’s total revenue pie (for 4Q 2009) and saw a 119% year-on-year revenue growth. General Equipment rental suffered a decline due to the discontinuance of the waste management division and heavy haulage New South Wales Division.

As reported by the Company, the extended wet season in North Queensland in 4Q 2009 also affected sales. Interesting to note is that for the first time, the % contribution from equipment sales fell below that of crawler crane rental, registering 26.9% compared to 34.9%, which very clearly shows the shift from equipment sales (a low margin business division) to crane rental (a much higher margin business division). Read more...

Further Reading

Tat Hong – FY 2009 Financial Analysis and Review Part 1

From the above diagram and breakdown, it can be seen that for 4Q 2009, crane rental took up a more significant portion of revenues at 40.6% (combining crawler and tower crane rentals), compared to just 22.6% a year ago. Granted, this was based on a lower revenue base (total revenue dipped from S$183.7 million to S$110.7 million for 4Q 2009 against 4Q 2008, a 40% drop) but it illustrates how Tat Hong are slowly but surely moving towards a “rental” business model, and how it can help to sustain revenues and cash flows.

If we dig deeper, it can be seen that crawler crane rental revenues barely dipped for 4Q 2009 compared to a year ago, with revenues holding steady at S$38.6 million. By contrast, sale of cranes fell 68% as the global downturn sucked up financing for companies and left them high and dry and unable to commit to more capex, hence hurting this division severely. Revenues from sale of cranes for 4Q 2009 fell from S$92.6 million to just S$29.7 million, and from the looks of things, is likely to worsen even further for 1Q 2010. Tower cranes, on the other hand, show good growth prospects as they now occupy 5.7% of Tat Hong’s total revenue pie (for 4Q 2009) and saw a 119% year-on-year revenue growth. General Equipment rental suffered a decline due to the discontinuance of the waste management division and heavy haulage New South Wales Division.

As reported by the Company, the extended wet season in North Queensland in 4Q 2009 also affected sales. Interesting to note is that for the first time, the % contribution from equipment sales fell below that of crawler crane rental, registering 26.9% compared to 34.9%, which very clearly shows the shift from equipment sales (a low margin business division) to crane rental (a much higher margin business division). Read more...

Further Reading

Tat Hong – FY 2009 Financial Analysis and Review Part 1