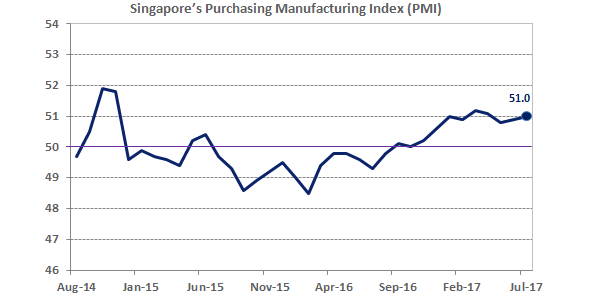

Singapore’s Purchasing Manufacturing Index (PMI), a key barometer of the Singapore manufacturing economy, has recorded 11 consecutive months of expansion.

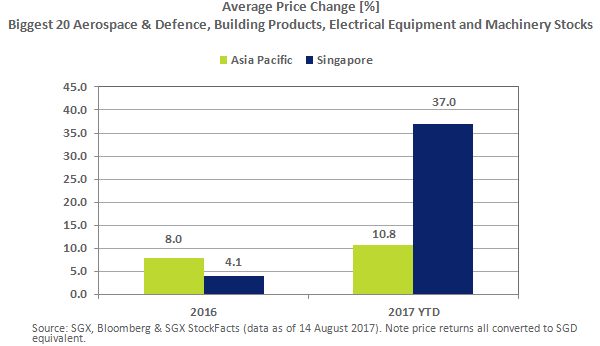

Singapore’s 20 largest capitalised stocks that represent manufacturing segments of the Capital Goods Industry have averaged a 37% price gain in the 2017 YTD, compared to an average 11% gain for the 20 largest of these stocks listed across Asia Pacific.

The three best performers among these 20 Capital Good stocks in the 2017 YTD were Starburst Holdings, Frencken Group and Yangzijiang Shipbuilding Holdings. All three stocks reported significant YoY growth in 1HFY17 net profit attributable to shareholders.

Index for Singapore’s Manufacturing Economy – 11 Consecutive Months of Expansion

Singapore’s Purchasing Manufacturing Index (PMI) rose to 51.0 in July 2017, and has been above the 50.0 expansion threshold since November 2016. The Singapore Institute of Purchasing & Materials Management (SIPMM) is scheduled to report the PMI for August on 4 September. SIPMM maintains that the Singapore PMI has become a key barometer of the Singapore manufacturing economy. As illustrated below the gauge generated an uptrend between February 2016 and July 2017, and has recorded 11 consecutive months of expansion.

Source: Singapore Institute of Purchasing & Materials Management (click

here). Note a reading of the Singapore Purchasing Managers’ Index (PMI) above 50 indicates that the manufacturing economy is generally expanding and that the economy is generally declining when the reading falls below 50.

Manufacturing-related Segments of the Capital Goods Industries

Capital Goods stocks make up as much as four-fifths of the market capitalisation of Singapore’s mega Industrials Sector. According to the Global Industry Classification Standard (GICS®) the Capital Goods Industry group is made up of seven different industries. Of the seven industries – there are four that have a manufacturing focus: Aerospace & Defence, Building Products, Electrical Equipment and Machinery.

Note outside of these four manufacturing-related segments for the Capital Goods Industry (within the Industrials Sector) there are other stocks that are represent manufacturing sub-sectors in the Consumer, Information Technology and Health Sectors.

The 20 largest capitalised stocks in Singapore that represent these four manufacturing-related segments in the Capital Goods Industry have averaged a 37.0% price gain in the 2017 year-to-date, following on from an average 4.1% price gain in 2016.

Comparative Regional Performance

Across Asia Pacific, the 20 largest capitalised primary-listed stocks of these four segments within the Capital Goods Industry (which includes Singapore Tech Engineering) have averaged an 10.8% price gain in the 2017 year to date, which followed an 8.0% price gain in 2016. There are now six China stocks that help to make up Asia-Pacific’s 20 largest capitalised primary-listed stocks of these four segments, which is up from one stock 10 years ago.

The comparative performance of both Asia Pacific’s Singapore’s 20 largest stocks of the four manufacturing-related segments of the Capital Goods Industry are tabled below.

As is currently the case in Singapore, the majority of Asia Pacific’s 20 largest stocks representing these four segments are Machinery plays. There are just the two Aerospace & Defense stocks amongst these 20 Asia Pacific stocks – Singapore Tech Engineering and AECC Aviation Power which is listed in China. While both stocks have similar market capitalisation, Singapore Tech Engineering has outperformed in both 2016 and 2017.

20 Biggest Stocks representing Manufacturing Segments in the Capital Goods Industry

As noted above, the 20 largest capitalised stocks in Singapore that represent the four manufacturing-related segments in the Capital Goods Industry have averaged a 37.0% price gain in the 2017 year-to-date. The Machinery segment was the most consistent performer in 2016 and the 2017 year-to-date, with the 13 stocks (of the 20) averaging a 7.7% price gain in 2016 and following on with an average 38.3% in the 2017 year-to-date. To see more details on each of the stocks below, click the stock name to see the full profile in SGX StockFacts.

Source: SGX, Bloomberg & SGX StockFacts (data as of 14 August 2017). Please note stocks tabled above are listed on the Mainboard or Catalist.

As detailed in the table above, the majority of the gains of the 20 stocks occurred in the first half of 2017, which coincided with expansion in Singapore’s Manufacturing Economy as gauged by the PMI. In addition Gross Domestic Product (GDP) came in stronger than expected – with GDP year-on-year (YoY) growth of 2.5% in the first quarter and 2.9% in the second quarter of 2017.

Of the 20 stocks, the three best performing stocks in the 2017 year-to-date were Starburst Holdings, Frencken Group and Yangzijiang Shipbuilding Holdings.

Starburst Holdings

On 11 August, Starburst Holdings reported it returned to profitability, achieving net profit attributable to shareholders of S$0.6 million for 1HFY17, compared to a net loss attributable to shareholders of S$2.1 million in 1HFY16. Starburst Holdings is a Singapore-based engineering group specialising in the design and engineering of firearms-training facilities – to see more information on its recent results click

here.

Frencken Group

On 10 August Frencken Group reported its net profit attributable to equity holders for 1HFY17 increased substantially to S$22.9 million, up 219.8% from S$7.2 million in 1HFY16. Excluding the net gain on disposal of subsidiaries, the high-tech capital and consumer equipment service provider, posted a 77.6% increase in net profit to S$12.7 million in 1HFY17 from S$7.2 million in 1HFY16.

In its business segment outlook, Frencken Group noted that the overall revenue of the automotive segment is expected to be lower in 3QFY17 as compared to 3QFY16, owing mainly to the disposal of shares in Precico Electronics Sdn Bhd with effect from 1 April 2017. For more information click

here.

Yangzijiang Shipbuilding (Holdings)

On 7 August, Yangzijiang Shipbuilding (Holdings) reported 1HFY17 net profit attributable to equity holders increased to RMB 1.387 billion, up 61% YoY, from RMB 863.377 million in 1HFY16. As discussed in the press release (click

here) the global shipbuilding market continued to recover in the first half of 2017, especially in some segments, such as dry bulk carrier, supported by the higher volume of iron ore transportation and the ease of overcapacity, while new shipbuilding demand for containership remained weak.

SGX My Gateway

SGX’s investor education portal with market, product and investment information and events. Sign up now at

sgx.com/mygateway to receive our investment updates and economic calendar.

This document is not intended for distribution to, or for use by or to be acted on by any person or entity located in any jurisdiction where such distribution, use or action would be contrary to applicable laws or regulations or would subject Singapore Exchange Limited (“SGX”) to any registration or licensing requirement. This document is not an offer or solicitation to buy or sell, nor financial advice or recommendation for any investment product. This document is for general circulation only. It does not address the specific investment objectives, financial situation or particular needs of any person. Advice should be sought from a financial adviser regarding the suitability of any investment product before investing or adopting any investment strategies. Use of and/or reliance on this document is entirely at the reader’s own risk. Further information on this investment product may be obtained from www.sgx.com. Investment products are subject to significant investment risks, including the possible loss of the principal amount invested. Past performance of investment products is not indicative of their future performance. Examples provided are for illustrative purposes only. While each of SGX and its affiliates (collectively, the “SGX Group Companies”) have taken reasonable care to ensure the accuracy and completeness of the information provided, each of the SGX Group Companies disclaims any and all guarantees, representations and warranties, expressed or implied, in relation to this document and shall not be responsible or liable (whether under contract, tort (including negligence) or otherwise) for any loss or damage of any kind (whether direct, indirect or consequential losses or other economic loss of any kind, including without limitation loss of profit, loss of reputation and loss of opportunity) suffered or incurred by any person due to any omission, error, inaccuracy, incompleteness, or otherwise, any reliance on such information, or arising from and/or in connection with this document. The information in this document may have been obtained via third party sources and which have not been independently verified by any SGX Group Company. No SGX Group Company endorses or shall be liable for the content of information provided by third parties. The SGX Group Companies may deal in investment products in the usual course of their business, and may be on the opposite side of any trades. SGX is an exempt financial adviser under the Financial Advisers Act (Cap. 110) of Singapore. The information in this document is subject to change without notice. This document may only be onward disseminated by the recipient wholly or in part if its content is attributed to SGX. This document shall not otherwise be reproduced, republished, uploaded, linked, posted, transmitted, adapted, copied, translated, modified, edited or otherwise displayed or distributed in any manner without SGX’s prior written consent.”