This post is a continuation from my article on ComfortDelGro's valuation yesterday.

Previous article: ComfortDelGro: A safe entry price?

In my previous article, I had arrived at a valuation for CDG's taxi business segment, using its net asset value. As some users on InvestingNote have pointed out, using CDG's net asset value may not be the most appropriate valuation method, as the vehicles may not be liquidated at book value.

Based on the feedback, I've revised my calculations, to take into account the projected fall in taxi fleet numbers, revenue, profit margins and earnings.

Valuation of Taxi Segment

Here's how I arrived at my updated valuation for CDG's taxi business, along with some key assumptions:

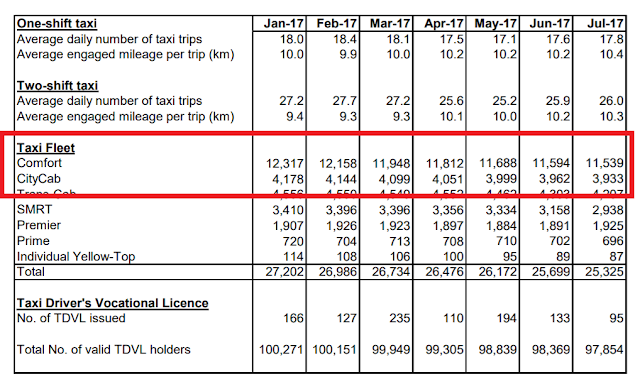

Source: LTA website

As per LTA statistics, the CDG's taxi fleet numbers have been steadily declining month-on-month for the past year. In July 2016, CDG had 17,044 taxis, and one year later, this figure dropped to 15,472 as of July 2017 -...

{kind=link}