The IT Sector was the strongest of Singapore's Sectors in September, with market capitalisation weighted total returns of 3.9%. This was followed by the Energy Sector with a 2.6% return and the Consumer Discretionary Sector with a 1.1% return.

Overnight, SIPMM reported that Singapore’s electronics cluster’s PMI posted a reading of 53.6 in September, up from August’s reading of 53.2, its 14th straight month of expansion and the highest recorded reading since July 2010.

In addition to being the largest capitalised stock of the IT Sector, Venture is currently the biggest stock on the STI Reserve List by full market capitalisation. This Reserve List is used in the event that one or more of the STI constituents are deleted prior to the next quarterly review.

Singapore’s Information Technology (“IT”) again led Sector performances in September based on average market capitalised weighted total returns. This was the sixth time in 12 months that the IT Sector had led the broad market. The gains in Singapore’s IT Sector also coincided with the Electronics Sector PMI expanding to higher levels in September.

Electronics Sector PMI

Last night the Singapore Institute of Purchasing & Materials Management (“SIPMM”) published the Singapore Purchasing Managers’ Index (PMI) in addition to the Electronics Sector PMI for the month of September. The full report can be read

here.

For the Electronics Sector PMI, SIPMM noted that the Electronics Sector PMI increased 0.4 points from the previous month to post a higher expansion reading at 53.6 in September. This is the highest recorded reading since July 2010, and the electronics manufacturing sector has now recorded its 14th month of consecutive expansion. A reading above 50 points to growth in the sector; one below 50 indicates contraction.

Recent Performance of 20 Largest Capitalised IT Stocks

The 20 largest capitalised stocks of Singapore’s IT Sector averaged a 1.0% total return in September. Venture Corporation generated an 11.7% gain and made up 35% of the Sector’s total market capitalisation of S$14.2 billion on 29 September. Hence the 3.9% market-capitalisation weighted gains of the Sector in September were highly impacted by Venture’s performance.

Over the past nine months these 20 stocks have averaged a 66.3% price gain with reinvested dividends boosting that average return to 73.0%. To see the profile of each stock in SGX StockFacts click on the stock name below.

Source: Bloomberg & SGX StockFacts (data as of 29 September 2017)

The best performing stock of the 20 biggest IT stocks in September was Micro-Mechanics Holdings. Micro-Mechanics designs, manufactures and markets high precision parts and tools used in process-critical applications for the wafer-fabrication and assembly processes of the semiconductor industry.

On 28 August Micro-Mechanics Holdings reported that its net profit jumped 24.2% to a record level of S$14.8 million for its FY17 ended 30 June 2017. The company also noted revenue growth of 11.7% to S$57.2 million, an expansion in gross profit margin to 57.4% and a tight rein on expense structure. For more details click

here.

As noted in the 2017 Annual Report (click

here) the Group began began in 1983 with a small factory in Singapore, and has grown steadily to become a publicly listed corporation with a global presence. Today, Micro-Mechanics serves a worldwide base of customers from five manufacturing facilities located in Singapore, Malaysia, China, the Philippines and the United States, and a direct sales presence in Taiwan and Europe.

STI Reserve List

Venture Corporation is now the biggest stock on the STI Reserve List by full market capitalisation. As of the 2 October close, Venture’s current market capitalisation was S$5.116 billion [up from S$4.997 billion on 29 September] compared to Suntec REIT’s current market capitalisation of S$4.954 billion. Note the relative market capitalisations of stocks generally change on a day to day basis with the price of a stock.

The STI Reserve List will be used in the event that one or more of the STI constituents are deleted during the period up to the next quarterly review. As detailed in the STI Ground Rules (click

here) when a company is going to be removed from the STI the vacancy will be filled by selecting the highest ranking security by full market value in the Reserve List as at the close of the index calculation two days prior to the deletion. There are further qualifications for the framework of the STI Reserve List in the case as Mergers, Restructuring and Complex Takeovers as described in Section 6.4 of the STI Ground rules.

The other four stocks of the STI Reserve List are Suntec REIT, Mapletree Commercial Trust, Keppel REIT and SIA Engineering.

Indicative Market-Capitalisation Weighted Total Returns

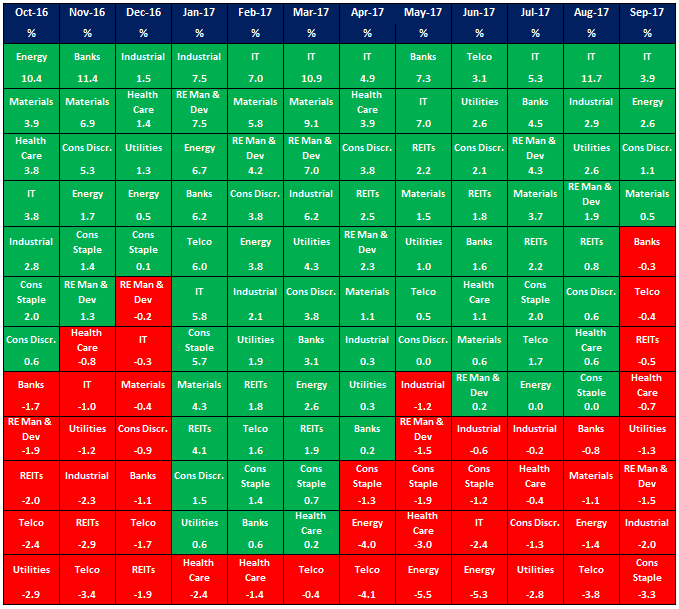

As illustrated in the Sector heatmap below, the IT Sector was again the strongest sector in September with indicative market capitalisation weighted total returns of 3.9%. This was followed by the Energy Sector with a 2.6% return and the Consumer Discretionary Sector with a 1.1% return. The IT Sector has been the strongest of the Sectors for six of the past 12 months.

Source: SGX StockFacts & Bloomberg. For monthly data, the Indicative GICS® Sector and Industries performance is weighed to market cap at each month end, in SGD and includes reinvested dividends.

The indicative sum of the best performing sector for each of the past 12 months was 84.9%. As illustrated below, the 84.9% total return, weighed to market capitalisation, started with the Energy Sector returning 10.4% in October 2016 and ended with the IT Sector adding 3.9% in September 2017.

Meanwhile, the combined decline for the least performing Sector of each of the last 12 months was 37.2%. By comparison, over the 12 months the STI generated a total return of 16.0%. Note the aforementioned indicative returns does not include any transactions fees which would be associated with the sector rotation.

This document is not intended for distribution to, or for use by or to be acted on by any person or entity located in any jurisdiction where such distribution, use or action would be contrary to applicable laws or regulations or would subject Singapore Exchange Limited (“SGX”) to any registration or licensing requirement. This document is not an offer or solicitation to buy or sell, nor financial advice or recommendation for any investment product. This document is for general circulation only. It does not address the specific investment objectives, financial situation or particular needs of any person. Advice should be sought from a financial adviser regarding the suitability of any investment product before investing or adopting any investment strategies. Use of and/or reliance on this document is entirely at the reader’s own risk. Further information on this investment product may be obtained from www.sgx.com. Investment products are subject to significant investment risks, including the possible loss of the principal amount invested. Past performance of investment products is not indicative of their future performance. Examples provided are for illustrative purposes only. While each of SGX and its affiliates (collectively, the “SGX Group Companies”) have taken reasonable care to ensure the accuracy and completeness of the information provided, each of the SGX Group Companies disclaims any and all guarantees, representations and warranties, expressed or implied, in relation to this document and shall not be responsible or liable (whether under contract, tort (including negligence) or otherwise) for any loss or damage of any kind (whether direct, indirect or consequential losses or other economic loss of any kind, including without limitation loss of profit, loss of reputation and loss of opportunity) suffered or incurred by any person due to any omission, error, inaccuracy, incompleteness, or otherwise, any reliance on such information, or arising from and/or in connection with this document. The information in this document may have been obtained via third party sources and which have not been independently verified by any SGX Group Company. No SGX Group Company endorses or shall be liable for the content of information provided by third parties. The SGX Group Companies may deal in investment products in the usual course of their business, and may be on the opposite side of any trades. SGX is an exempt financial adviser under the Financial Advisers Act (Cap. 110) of Singapore. The information in this document is subject to change without notice. This document may only be onward disseminated by the recipient wholly or in part if its content is attributed to SGX. This document shall not otherwise be reproduced, republished, uploaded, linked, posted, transmitted, adapted, copied, translated, modified, edited or otherwise displayed or distributed in any manner without SGX’s prior written consent.”