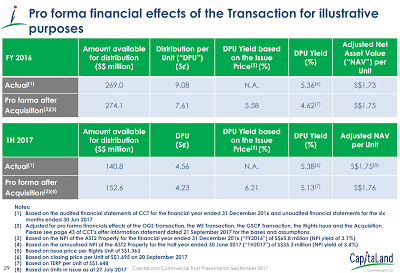

I made a mistake on CapitaLand Commercial Trust (CCT) rights issue! By now you would have come across the news - Capitaland Commercial Trust buys Asia Square Tower 2 for $2.09b. Although the acquisition is not yield-accretive (dividend yield decrease to 4.62% from 5.36%), KPO thought that it would still be a great idea to buy and hold CCT directly instead of the upcoming 3rd REIT ETF - Lion-Phillip S-REIT ETF.

The rights issue presented an excellent opportunity for me to become a shareholder at a price lower than the market price if I were to apply/oversubscribe to the rights! Technically, based on the theoretical ex-rights price (TERP) of $1.648 and a subscription price of $1.363, if I were to get my rights/baby shares at any price lower than $0.285 ($1.648 - $1.363), I would have the chance to get it lower than the market/TERP. Hence, I queued at $0.28 and got...

{kind=link}