- DBS, OCBC and UOB averaged 8% gains in April-to-date, bringing average YTD total returns to 14%, and 12 month average total returns to 50%. April has seen the three banks trade at all-time highs, with DBS recently trading at a high of S$30.00.

- The three banks currently average a 1.5x P/B, above the 10 year average P/B, and in-line with the 20 year average. In the YTD institutional investors were net buyers of the three banks, with inflows totalling S$1.12 billion, following net inflows of S$3.39 billion in 2017.

- FY17 Net Profit of the three banks totalled S$11.9 billion. Recent Annual Reports detailed multiple initiatives in FY17, with all three banks reporting growth of wealth management services, digital innovations and alignments with the Belt & Road Initiative (BRI).

Singapore’s listed Bank Sector consists of DBS Group Holding ("DBS"), Oversea-Chinese Banking Corporation ("OCBC") and United Overseas Bank ("UOB"). These stocks are respectively ranked first, fourth and eighth largest stocks in South East Asia by market capitalisation.

The three banks’ combined market capitalisation stands at S$183 billion. As of the end of March the three stocks made up 41.6% of the Straits Times Index. This combined weightage is up from 39.8% at the end of January as discussed in February (click

here for more).

Financial Returns & Valuations

Combined, the FY17 Net Profit of the three banks totalled S$11.9 billion with the average Return-on-Equity (“ROE”) for FY17 at 10.4%. DBS reported an ROE of 9.7% as total allowances increased due to the accelerated NPA recognition in the O&G support services sector. OCBC reported a ROE of 11.2% and UOB reported an ROE of 10.2%.

The three banks currently average a Price-to-book ratio (“P/B”) of 1.5x, above their 10 year average P/B of 1.3x and in-line with the 20 year average.

In the 2018 year through to 25 April, institutional investors were net buyers of the three banks, with inflows totalling S$1.12 billion, following net inflows of S$3.39 billion in 2017.

Singapore Banks saw All-Time Highs in April

DBS, OCBC and UOB averaged 8.1% gains in April-to-date, bringing average YTD total returns to 14.4%, and 12 month average total returns to 50.0%.

Singapore Banks saw All-Time Highs in April

DBS, OCBC and UOB averaged 8.1% gains in April-to-date, bringing average YTD total returns to 14.4%, and 12 month average total returns to 50.0%. The STI has added 4.2% in the month through to 25 April, to bring its year-to-date total return to 5.4%, and 12 month total return to 16.4%.

This month has seen the three banks trade at all-time highs, with DBS notably trading at an all-time high of S$30.00 earlier this week. UOB’s all-time high at S$29.90 was reached on 19 April, and OCBC opened this morning at an all-time of S$13.80. To see more details on the performances of the three stocks click on the stock names in the table below.

| Name |

SGX Code |

Market Cap S$B |

25 April Closing Price |

Total Return YTD % |

12M Total return % |

Month to Date Return % |

P/B

(x) |

Dividend

Yield % |

| DBS Group Hldgs |

D05 |

76.3 |

29.770 |

19.8 |

62.7 |

9.1 |

1.6 |

3.1 |

| Oversea-Chinese Banking Corp |

O39 |

57.3 |

13.710 |

10.7 |

47.3 |

7.2 |

1.5 |

2.7 |

| United Overseas Bank |

U11 |

49.5 |

29.800 |

12.7 |

39.9 |

8.0 |

1.5 |

2.7 |

| Average |

|

|

|

14.4 |

50.0 |

8.1 |

1.5 |

2.8 |

Source: Bloomberg & SGX StockFacts (Data as of 25 April 2018)

Interest Income & the Rate Cycle

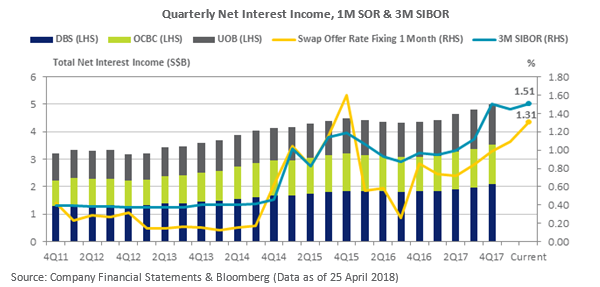

Net interest income basically represents the difference between revenue on its lending and the liabilities it pays to depositors. Combined, the quarterly net interest income for the three banks has gradually grown in recent years and has been consistently above S$4.0 billion for each quarter since the end of 2014.

This has coincided with gradual increases of interest rates as represented by the 1-month Swap Offer Rate (“SOR”) and 3-month Singapore Interbank Offered Rate (“SIBOR”) .

As illustrated in the chart below by the 1-month Swap Offer Rate (“SOR”) and 3-month Singapore Interbank Offered Rate (“SIBOR”) have also increased markedly since Dec 2014. This has coincided with moves in US interest rate expectations. The banks generally offer mortgages based on SIBOR rates, which are less volatile that the SOR, with the latter impacted by the USD/SGD exchange rate. As illustrated below the difference between the 1-month SOR and 3-month SIBOR widened in the fourth quarter of 2017, and has since narrowed.

The recently published FY17 Annual Reports also detailed multiple initiatives by the banks in FY17, with all three reporting growth of wealth management services, digital innovations and alignments with the Belt & Road Initiative (“BRI”).

Belt and Road Initiative

All three Annual Reports made reference to the BRI which is a mega-economic initiative with the potential of trade-related solutions to address underinvestment and infrastructure deficiencies in emerging economies. While strengthening trade and the region’s financial flows, the BRI aims to improve regional integration of some 50 countries. Within the Annual Reports:

- DBS highlighted its objective to capture opportunities from BRI cross-border mergers and acquisitions activity, noting Chinese companies continued to execute on acquisition strategies in 2017 as part of the BRI. DBS’ Institutional Banking Team noted it had captured these opportunities by connecting Chinese acquirers with prospective targets in Asia, providing tailored buy-side or sell-side advice, and supporting due diligence efforts and transaction negotiations. Its efforts in “helping Chinese enterprises expand overseas and for providing comprehensive financial services along the BRI” were recognised with DBS winning the inaugural “Best Regional Bank in Southeast Asia for Belt and Road Initiatives” by Asiamoney. For the full Annual Report click here.

- OCBC noted that Malaysia, Indonesia and Greater China the ASEAN economies are key beneficiaries of the expansion in global trade and deeper Asian economic integration, while China’s Belt and Road Initiative is expected to spur infrastructure development in the region. OCBC noted it had continued to build upon its strong foundation in Greater China, where it had more than 100 branches and offices in China, Hong Kong and Macao under OCBC Wing Hang. Furthermore, OCBC noted that following a successful decade of partnership with its 20%-owned associated company Bank of Ningbo, the bank signed another 10-year comprehensive strategic agreement that will focus on greater collaboration for our onshore and offshore initiatives. Xiamen was the city where OCBC first established its presence in China in 1925. For the full Annual Report click here.

- UOB highlighted it has increased its efforts in facilitating China-ASEAN business flows along the BRI through new partnerships with its new Kunming branch in Yunnan. As noted by UOB, Yunnan is a strategic node of the BRI which has recorded strong trade and investment flows between Hong Kong and Southeast Asian countries. UOB note its new Kunming branch is well-positioned to help the businesses of Southwest China with their cross-border expansion plans through onshore and offshore solutions. Furthermore it also complements UOB’s operations in West China’s Chengdu and Chongqing. For the full Annual Report click here.