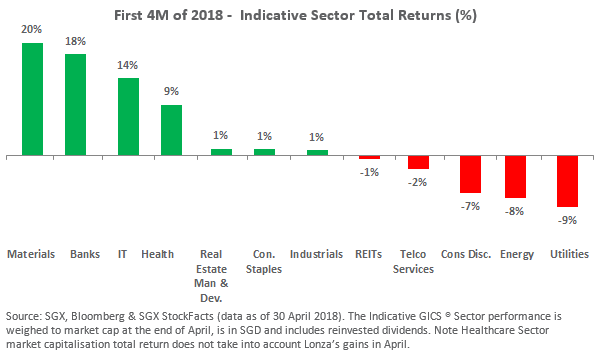

- The STI continued to outperform the region in April with Bank-led gains driving the STI’s total return to 7.1% over the first four months of 2018. This compared to an average decline of 0.1% for the benchmarks of Japan, Hong Kong and Australia.

- The three strongest sector segments in April included Banks, with capitalisation-weighted gains of 10.7%, followed by Telecommunication Services and Consumer Staples, both with capitalisation weighted returns of 4.0%.

- M1 led the performances of the largest Telecommunication Services stocks in April with a 7.6% total return, whilst Thai Beverage PCL and Sheng Siong Group led the largest Consumer Staples stocks with 9.6% and 9.7% respective returns.

During April, the Straits Times Index (“STI”) continued to outperform the region. The STI has now generated a 7.1% total return over the first four months of 2018. This compared to an average decline of 0.1% for the benchmarks of Japan, Hong Kong and Australia, which was also in line with the regional MSCI AC Asia Pacific Index.

Over the past 12 months the STI has added 17.6%, which compares to 13.9% for the MSCI AC Asia Pacific Index in SGD terms. For the month of April, the STI added 5.9%.

Over the past 12 months the STI has added 17.6%, which compares to 13.9% for the MSCI AC Asia Pacific Index in SGD terms. For the month of April, the STI added 5.9%.

As noted by MAS Monetary Policy Statement on 13 April (click

here) Singapore’s recent sectoral composition of growth has been uneven. The report stated that:

- Within manufacturing, the semiconductor segment has continued to expand at a strong pace, but the marine and offshore engineering industry remains subdued.

- In services, retail and food services saw some pullback in activity after the pickup in 4Q17 last year, while business services posted further growth.

- The financial services sector also recorded varying outturns across its segments, with both domestic and offshore lending outperforming.

Within the Singapore stock market, sector performances have also varied. The Banks and the Information Technology (“IT”) sector have continued to be amongst the best performing sectors in the year thus far as illustrated below. However, the IT sector saw it recent run in the year-to-date pole positions end in April, with the declines of Venture Corporation weighing the sector.

Strongest Stock Sectors in April

Strongest Stock Sectors in April

The strongest sector segment in the month of April was Banks with capitalisation-weighted gains of 10.7%. For more details on the recent gains by the three banks click

here. The strong performance of the Bank sector in April was followed by Telecommunication Services and Consumer Staples, both with capitalisation-weighted gains of 4.0%.

M1 led the performances of the largest of the Telecommunication Services stocks with a 7.1% gain in April. On 16 April, M1 reported the unaudited group financial results for its 1QFY18 (to 31 Mar) with highlights as follows:

- Service revenue increased 3.0% YoY to S$184.7 million, driven by higher fixed services and postpaid revenues.

- The growing corporate and government segment contributed 37% of service revenue and reported 19% YoY growth in 1QFY18.

- Net profit after tax was stable YoY at S$34.8 million. Compared to the preceding quarter, net profit after tax increased 8.3%.

For more details click

here.

Thai Beverage PCL and Sheng Siong Group led the largest Consumer Staples stocks with 9.6% and 9.7% respective returns. On 27 April, Sheng Siong Group reported its net profit for 1QFY18 grew 6.6% YoY to S$18.3 million. Other reported highlights included:

- Revenue increased 5.1% YoY to S$228.3 million in 1QFY18 mainly contributed by new stores and comparable same store sales.

- Gross profit margin improved to 26.2% in 1QFY18 from 25.2% in 1QFY17.

- The Group reported it will continue with its efforts in expanding the network of outlets in Singapore especially in areas where its potential customers reside.

For more details click

here.

The tables below detail the relative performances of the Banks, the four largest Telecommunication Services stocks and the 10 largest capitalised Consumer Staples stocks. To see more details on each stock in SGX StockFacts, click on the stock name.

| Banks |

SGX Code |

Market Cap S$B |

30 April Closing Price |

Total Return April % |

Total Return YTD % |

12M Total return % |

10 Year Return % |

Dvd Ind Yld % |

| DBS |

D05 |

79.1 |

30.840 |

12.1 |

24.1 |

64.3 |

158.7 |

3.0 |

| OCBC |

O39 |

57.7 |

13.800 |

7.6 |

11.4 |

45.6 |

128.0 |

2.7 |

| UOB |

U11 |

50.1 |

30.140 |

12.0 |

16.5 |

43.4 |

115.7 |

2.7 |

| Average |

|

|

|

10.6 |

17.3 |

51.1 |

134.1 |

2.8 |

Source: Bloomberg & SGX StockFacts (Data as of 30 April 2018)

| Four Largest Capitalised Telecommunication Stocks |

SGX Code |

Market Cap S$B |

30 April Closing Price |

Total Return April % |

Total Return YTD % |

12M Total return % |

10 Year Return % |

Dvd Ind Yld % |

| Singtel |

Z74 |

57.5 |

3.520 |

4.5 |

-1.4 |

-0.7 |

48.7 |

5.0 |

| StarHub |

CC3 |

3.9 |

2.270 |

0.4 |

-18.9 |

-13.4 |

41.7 |

7.1 |

| NetLink NBN Trust |

CJLU |

3.2 |

0.810 |

-0.6 |

-3.0 |

N/A |

N/A |

N/A |

| M1 |

B2F |

1.7 |

1.810 |

7.6 |

5.2 |

-11.2 |

72.1 |

6.3 |

| Average |

|

|

|

3.0 |

-4.5 |

-8.4 |

54.1 |

6.1 |

Source: Bloomberg & SGX StockFacts (Data as of 30 April 2018)

Source: Bloomberg & SGX StockFacts (Data as of 30 April 2018)

Sector and Industry Moves in April

Other highlights at the sector level included:

- The two Consumer sectors, Consumer Discretionary and Consumer Staples, were amongst the five strongest sectors in April, the first time both had been ranked among the five best performers since November 2016.

- During April, the eight stocks that make up the Food & Staples Retailing segment within the Consumer Staples sector generated capitalisation weighted gains of 4.2%.

- On the Consumer Discretionary side, the 30 stocks that make up the Hotels, Restaurant and Leisure segment generated a market capitalisation weighted total return of 4.0%, whilst the Media segment generated a 3.6% gain by the same measure.

- While the Industrial sector performances remain subdued on the marine and capital goods front in April, the 25 Transportation stocks generated a 4.7% market capitalisation weighted total return for the month.

- IT was the least performing sector, with Venture declining 25.5% in April, having a significant impact on the sector. Venture’s decline in April pared its year-to-date gain to 2.4%. The dozen stocks that make up the Semiconductor segment of the IT sector generated a market capitalisation weighted decline of 8.1%, paring their year-to-date gain by the same measure to 19.8%. Meanwhile the seven stocks that represent the IT Services industry generated market capitalisation weighted returns of 6.2% in April.

April Indicative Sector Performances

As noted above, the STI generated a 5.9% total return in April, following on from a 2.6% decline in March. As illustrated in the

Sector Heatmap below, IT was the least strongest of the sectors in April, whilst Banks was the strongest segment in April with a 10.7% market capitalisation total return.

The indicative sum of the best performing sector for each of the past 12 months was 96.5%. As illustrated above, the 96.5% total return, weighed to market capitalisation, started with the Banks segment returning 7.3% in May 2017 and ended with the Banks segment adding 10.7% in April 2018.

The combined decline for the least performing sector of each of the last 12 months was 55.6%. By comparison, over the 12 months the STI generated a total return of 17.6%. Note this does not include any transactions fees which would be associated with sector rotations.

Defensive sectors were amongst the least performing sectors for nine of the 12 past months whilst Cyclical sectors were amongst the strongest performing sector for 10 of the past 12 months.