Singapore O&G (SOG), one of my highest conviction holdings reported bad headline results on Friday night. But after digging in, the good news seem to outweigh the bad.

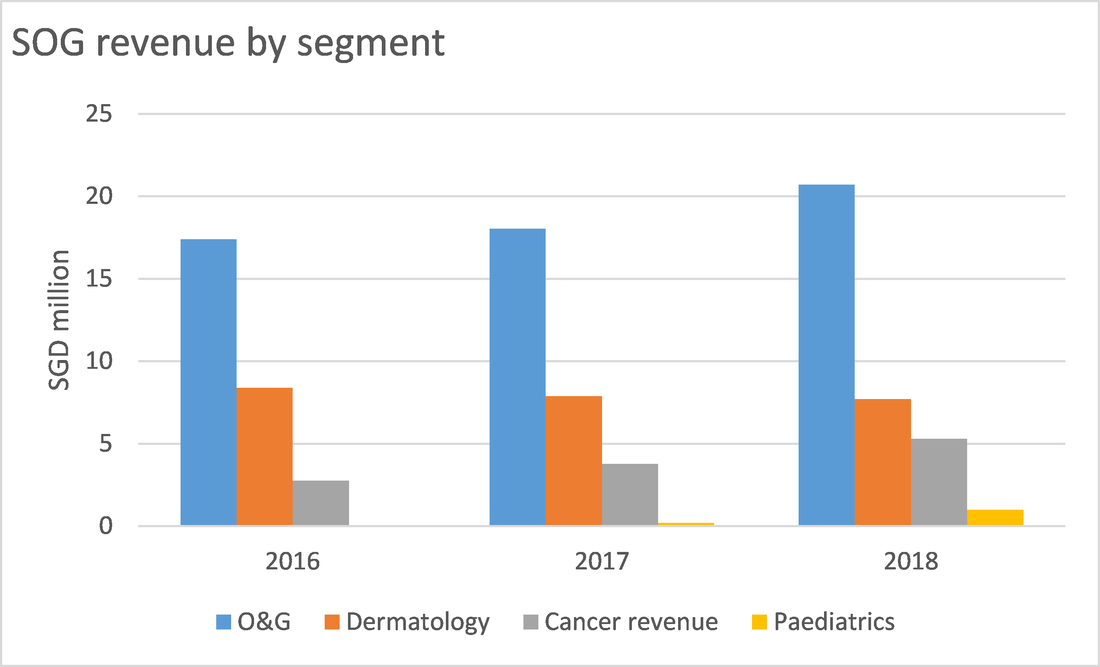

4Q18 revenue grew 10% year on year, recurring net profit was up 39% year on year, operating cash flow was up and the final dividend grew 1%. However, reported net profit fell 98% because of a goodwill charge on the company’s dermatology segment. The dermatology segment has been performing poorly since its 2016 acquisition with revenue and net profit falling every year due to fierce foreign competition. SOG still has SGD24 million of goodwill related to the dermatology acquisition on its books but a complete write-down seems unlikely with the revenue decline slowing in 2018.