One of the biggest counter-argument to the safe-withdrawal-rate way of deriving your retirement income is that most of us do not spend like this in reality.

Our real-life spending tends to go up and down and seldom stays constant. So it is quite hard to accept that if we are given $40,000 that is inflation-adjusted, we will diligently spend all.

However, you can think of this as similar to a non-guaranteed endowment, whose value will fluctuate but will give you a consistent income. It is up to you to decide whether you should spend it.

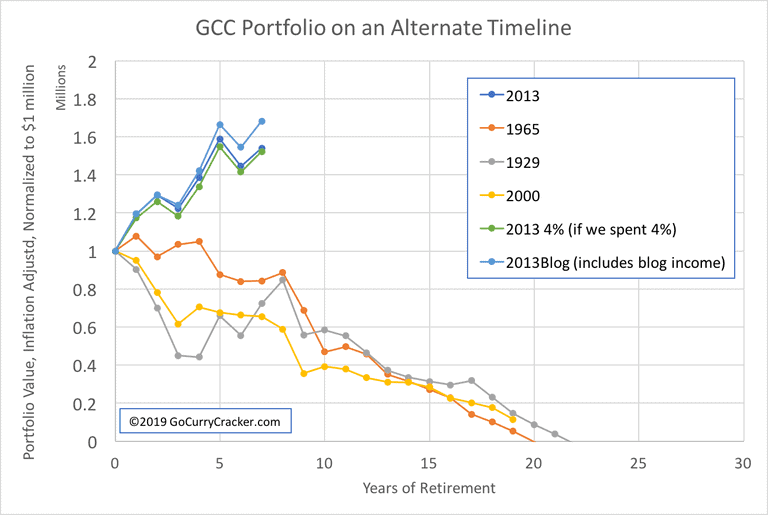

Go Curry Cracker has a good article this week that takes us through how we would spend our money if we are living in another parallel universe.

There are usually 2 methods of how people validate if a particular retirement method is robust, Monte Carlo simulation, or backtest with historical returns data.

However, they are

...