Sheng Siong is expected to report its 3Q19 results around 30 October. The company, with its defensive business model, has generally been well-liked by the market, with the exception of Maybank, which currently rates the counter a sell.

Despite current market volatility induced by US-China trade tension, Sheng Siong’s domestic grocery business has been relatively unaffected.

The company’s 1H19 performance had been credible, with net profit of SGD37.8m, 6.8% higher than 1H18 and generally within the street’s expectations.

For 2019, the market is expecting Sheng Siong to generate net profit of between c.SGD75m to c.SGD77m, representing approximately 6-9% YoY improvement.

Table of Contents

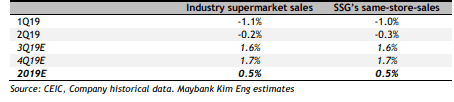

What the market might be looking out for in its 3Q19 resultsIf Sheng Siong manages to generate net profit growth of c.5-8%, that should be generally in-line with market expectations and we should expect the counter’s share price to maintain steady with

...