My mum had surgery recently in a private hospital. She stayed in a single bed for 3 nights and the estimated bill came up to $22,000. She has a private MediShield with AIA but no rider. This means that she has to pay a total of $5,350 (deductible: $3,500, co-insurance: 10%) which I believe will be payable using MediSave or a combination of MediSave and cash. I did not have to pay any amount upfront because the insurer has a letter of guarantee. However the cost of the pre and post hospitalisation e.g. follow up checks and scans were not included and I will have to pay this amount upfront but 90% of the cost is claimable.

I am thankful that the surgery went smoothly and bearing the discomfort on the first night, there were no complications. I hope that this incident will serve as a reminder to my parents not to neglect their health and buff up their own financial security. Whenever I mention about financial planning, they will brush it aside saying that nothing will happen to them and I do not have to worry. However, reality is when something unfortunate happen, it is sudden and it comes at a bad timing – in my case my household expenses are increasing. Also, it is not only about themselves, other family members will have to chip in to take care of them.

During the first few days when my mum was hospitalised, I told my parents not to worry about the cost and to focus on getting well first. I am fortunate that there were already some financial plans in place prior to the surgery which kept the cost manageable. However, there are still lessons to be learnt to further improve the safety net for my parents.

With the rising cost of private MediShield, I have been thinking of downgrading even before this incident. It is a no brainer to downgrade if I look at the cost alone but there are several intangible factors to consider first.

Waiting Time

I have naturally heard of the long waiting time in public hospitals and I have also personally experienced it first hand. MOH has compiled a

statistic on the waiting time in government hospitals. The waiting time is about 3 hours max (excluding NTFGH) and is computed from the time "Decision by doctor to admit patient" to the "Time patient exits EMD” (to go to inpatient ward). My interpretation is that does not include the waiting time to see the doctor, going for scans/tests and waiting for the results. In my mum's case, she consulted a private GP on Monday night, saw the specialist the following morning, did her scan, got her results and was operated the same day.

I intend to downgrade the plan to a public hospital (A class ward and below) because I want my parents to be able to choose their preferred specialist. My preferred public hospitals are SGH and TTSH and it helps that AIA has a

list of doctors there. Some of the perks include "Secure an appointment with a specialist within 3 working days" and " Preferential 20% off AQHP outpatient consultation fees". I hope that by going to the public hospital as a private patient, the waiting time will be more manageable.

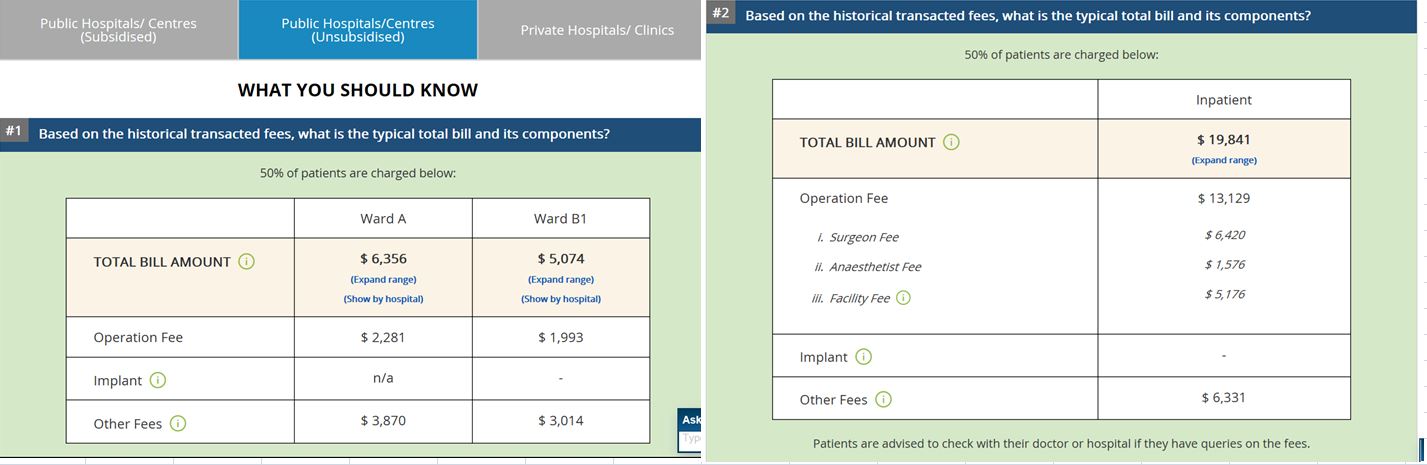

Cost of a patient in Private Hospital VS private patient in Public Hospital

By choosing a specialist, my parents will be classify as a private patient i.e. they will not have any subsidies. They will also be limited to either the A class ward (1 bedded room) or B1 class ward (6 bedded room). Surprisingly, the deductible and co-insurance for the private and public A class ward are the same. However is the cost of treatment as a private patient in Public Hospitals cheaper than Private Hospitals?

[caption id="attachment_1400149" align="alignnone" width="1712"]

A Class Ward Room Rates[/caption]

The A class ward room rates in SGH and TTSH are cheaper than all private hospitals except Mount Elizabeth Novena Hospital by at least $100 per day. If one is warded for an extended period of time or in the Intensive Care or High Dependency ward, the cost can add up very quickly.

In addition, MOH has a

website that compares the total hospitalisation fees in both public (subsided and non-subsidised) and private hospitals.

There are several surgical procedures to choose from. As I could not find my mum's surgical procedure, I decided to check on the cost of the appendix surgery as I had one in a private hospital a few years back. If my memory serves me correctly, the total cost of my pin-hole appendix surgery and hospitalisation cost about $30,000.

[caption id="attachment_1400150" align="aligncenter" width="1427"]

Fee Benchmarks and Bill Amount Information Lower abdomen, removal of appendix (simple)[/caption]

Source:

https://www.moh.gov.sg/cost-financing/fee-benchmarks-and-bill-amount-information/Details/SF849A—1

Based on the benchmark, a procedure without complications in A class ward in a public hospital is three times cheaper than a private hospital.

It is a foregone conclusion that even as a private patient in a public hospital, the cost is still very much cheaper than a private hospital.

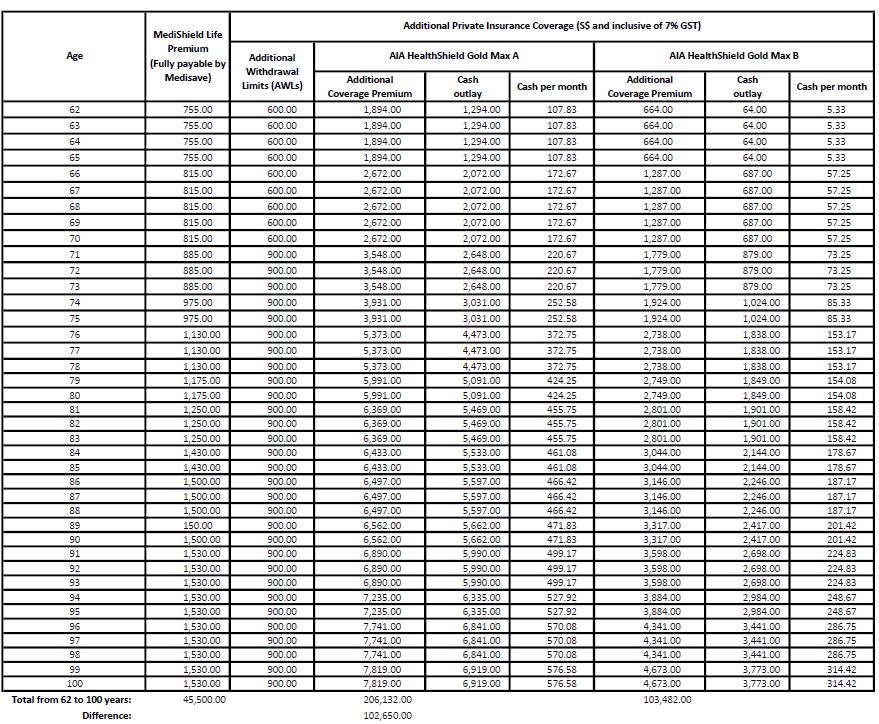

How much premiums will my parents save?

[caption id="attachment_1400151" align="aligncenter" width="879"]

AIA HealthShield Gold[/caption]

If I were to downgrade now, I will save $102,650.00 per person or $205,300.00 in premiums if my parents live till 100 years old. Affordability is also an important factor. While I am still able to pay for their premiums now, their premiums will rise as they get older while my own expenses will continue to increase. In addition, the insurers will probably revised the premiums upwards in the future due to escalating healthcare cost.

An interesting note is that MediShield Life Premiums will add up to $45,500.00. If you add this to Gold Max A, the premium for my parents is about $251,000 or $502,000 for the both of them!

My parents' MediSheild plan is only part of the comprehensive retirement plan that I am coming up for them. Any feedback or comments are welcome.

My parents are already downgrading their flat and my plan is for them to be self-sufficient when they retire i.e. be able to pay for their own bills, daily living expenses and some left over for travel and entertainment. The allowance from me will be an added bonus. With the financial load off their minds, they can look forward to enjoying their golden years as grandparents.

2.5