How to invest for income

A well-constructed portfolio of real estate investment trusts (REITs) is one simple way to build a substantial stream of passive income. Investors can also consider dividend stocks, bonds, and property to generate income. What to invest in ultimately depends on the degree of risk you're comfortable with, and the income you require. It helps to understand the various income-generating assets available to investors, as well as the things to look out for when evaluating them. REITs REITS invest in a portfolio of income generating assets such as shopping malls, offices, industrial parks, hotels and healthcare properties. With REITs, investors get to earn consistent dividend income either quarterly or semi-annually. Moreover, Singapore-listed REITs (S-REITs) are required to pay out at least 90% of their income as dividends.This is especially useful for investors who may want to use this payout to offset purchases, pay school fees, or fund yearly travels. In this lower-for-longer interest rate environment, yields offered by S-REITs are also seen as more attractive than bond yields. For instance, the average dividend yield of S-REITs is around 6.5% compared to the 10-year Singapore Savings Bonds (SSB) interest rate of 1.7% (SSB March 2020 issue). When choosing which REIT to include in your portfolio, consider the quality of the underlying REIT properties, the income stability of the REIT, its dividend track record, and the reputation of the REIT sponsor and management team. These factors can affect not just the share price of the REIT but also future dividend yields. Dividend Stocks Dividend stocks are the stocks of companies that pay out regular cash distributions to shareholders in the form of dividends. Do note however that not all companies pay a dividend, and companies may cut dividends in times of distress. Good dividend stocks are those that consistently pay dividends and increase the amount of dividends paid over time. Blue-chip stocks - shares from large, reputable companies the likes of SingTel and DBS - are a reliable option. Look for companies with a track record of growing profits, which consequently allow them to pay higher dividends over time. Ultimately, bear in mind that dividend stocks are still stocks. Their values may fluctuate dramatically in response to market conditions, so be sure to sufficiently diversify your selection of dividend stocks. Bonds When you purchase a bond, you’re essentially loaning money to a government entity or corporation. You receive interest payment on your loan on a fixed schedule, and when the loan term ends, you receive the amount you loaned back. This makes bonds an ideal choice for risk-averse income investors. There are two main types of bonds. Government bonds like the SSB are backed by the government and are considered one of the safest types of debt instruments available. Corporate bonds are issued by companies. While they tend to have higher interest rates than government bonds, there’s a higher risk of default as well. As the Hyflux crisis shows, it’s important for investors to continuously evaluate the financial health of the companies they invest in. To receive regular income from bonds, you can build a bond ladder by staggering the maturity dates or interest payment dates of several bonds. For instance, the SSB pays out dividends twice yearly and matures in 10 years. A SSB issued in August will pay out dividends in August and February; one issued in September will pay out dividends in September and March, and so on. This means that you can purchase 6 consecutive months of SSBs and enjoy monthly interest payments for the next 10 years! Property Investing in real estate is a hugely popular choice for Singaporeans. Renting out a condo unit is most common; it’s a way to earn monthly passive income while benefiting from capital gains if the price of the unit goes up. But investing in property is feasible only if you can afford the initial capital for a down payment and the monthly mortgage payments thereafter. The rental income you earn is not exactly passive either. You need time and effort to manage and maintain your property for your tenants, and costs associated with maintenance or repairs eat into your returns. REITs offer an affordable and cost-effective alternative for retail investors to start investing in real estate. Your capital and time commitment are lower, and you don’t get taxed on the dividends you earn from your REIT portfolio.Dividends Are Not Everything

Dividends are no doubt important to income investors but high dividends do not necessarily mean that an income investment is good. It’s equally important to consider the fundamentals of the company - revenue, profits, cash flow, business model - when evaluating whether dividend payouts will be sustainable in the long term. While it feels great to receive regular income from your investments, reinvesting dividends can actually supercharge your future dividend income if you don’t need the income now. Instead of receiving payouts, you end up purchasing more units of your investment each time dividends are paid. As you accumulate more assets, you are accelerating the power of compounding in your portfolio and boosting your long-term returns.Make $2,000 A Month With Income Investing

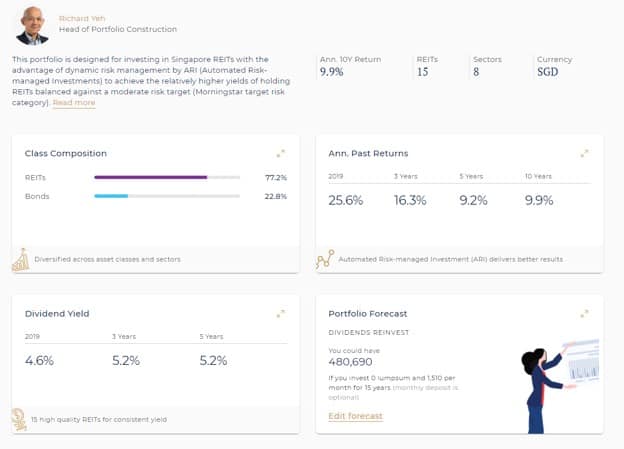

Assuming an average dividend yield of 5% per year, you will need an investment of $480,000 to start generating $24,000 in dividends annually. Yes, that’s close to half a million dollars, but don’t let the figure put you off. By starting with a smaller amount now, and reinvesting your dividends consistently, you can grow your total investment to $480,000 in 15 years. Let’s say you decide to invest in an income portfolio like Syfe’s REIT+ portfolio. It combines 15 S-REITs with Singapore government bonds to form a portfolio that provides a 5-year average dividend yield of 5.2%. Using the forecast tool on Syfe’s website, your investments can grow to $480,690 with an investment of $1,510 per month for 15 years, if you reinvest your dividends. 15 years later, you can choose to stop reinvesting your dividends and live on the dividends paid out as you pursue your dreams, be it early retirement or travelling around the world.

The Takeaway

Time is the friend of the income investor. If your goal is to achieve financial freedom within the next 20 years or so, start saving to invest. From automated savings to committing to a budget, saving more money is the bedrock of building passive income. After all, passive income is just a pipedream if you don’t have the means to generate it. And as you hit your 30s and 40s, chances are, you’re in your peak earning years, or will soon be reaching them. As your net worth grows, beware of lifestyle creep. Instead, funnel more cash into investing. By investing for income, you’re not just maximising the money you’ve worked hard to earn and save, but also providing yourself with a steady stream of cash you can tap on for your goals and aspirations.Syfe is a MAS-licensed digital wealth manager that helps investors grow their wealth through our proprietary Automated Risk-managed Investments (ARI) methodology.