1) Singtel Group’s Key Business Units

2) Historical Revenue and Profit Trends

3) How Cheap is Singtel? EV/EBITDA, P/E and Dividend Yield

4) What we think Singtel is worth

5) Potential Price Catalysts

Appendix 1: How big a catalyst would a Singtel-Grab Digital Bank license be?

Appendix 2: Broker valuation estimates for Singtel’s 35% stake in Telkomsel

The InvestQuest View:

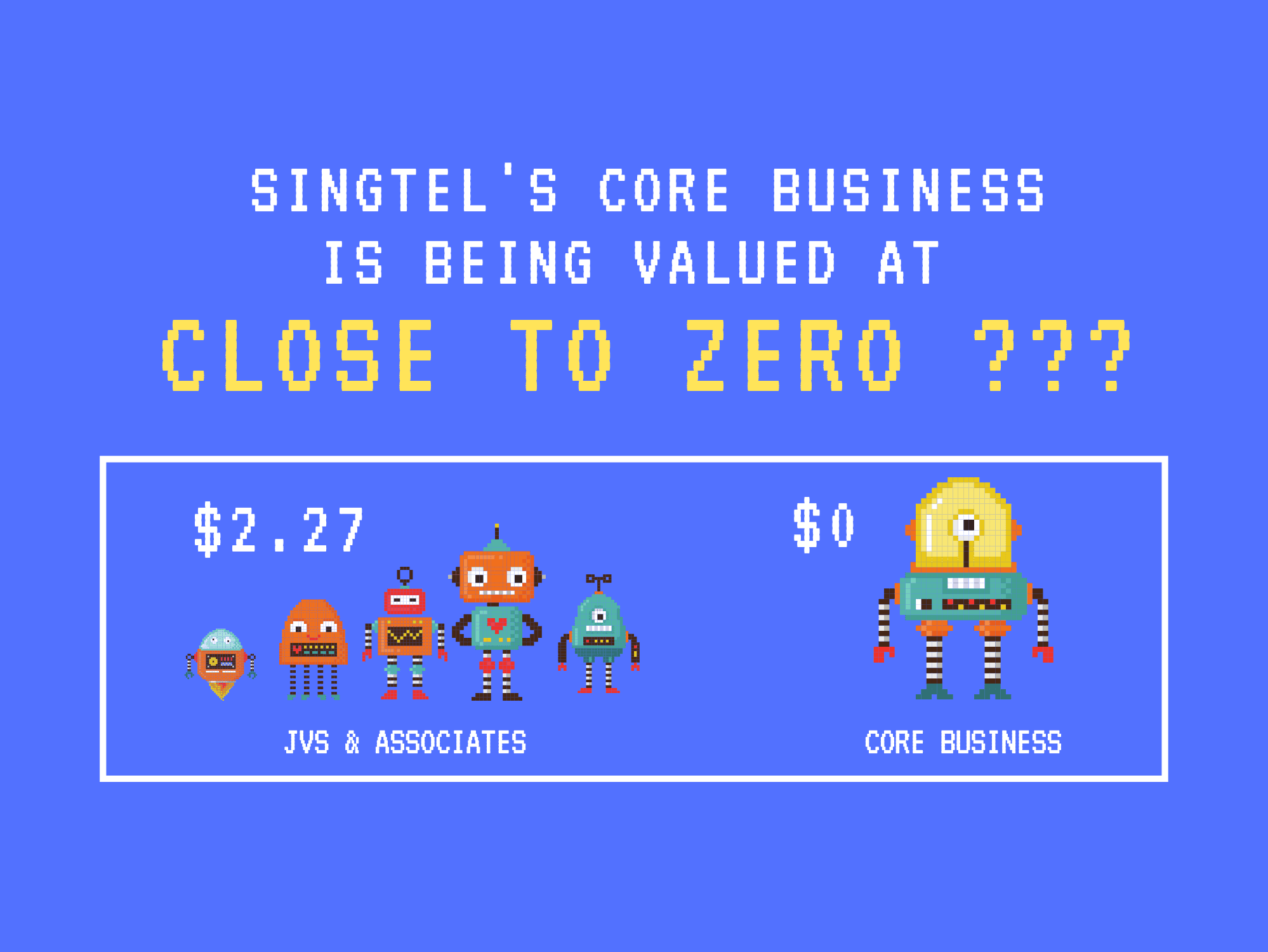

We have no doubt that Singtel is cheap. The value of its associates alone (which we estimate to be S$2.27), is already close to the Group’s current share price of S$2.39. Separately, our conservative valuation estimates point to a fair value of S$2.80, implying 17% potential upside from the current share price.

However, in order for the market to stop discounting Singtel, we believe that divestments in non-core assets (that can help support dividend payouts) and a convincing sequential improvement to Bharti’s financials will be helpful catalysts....