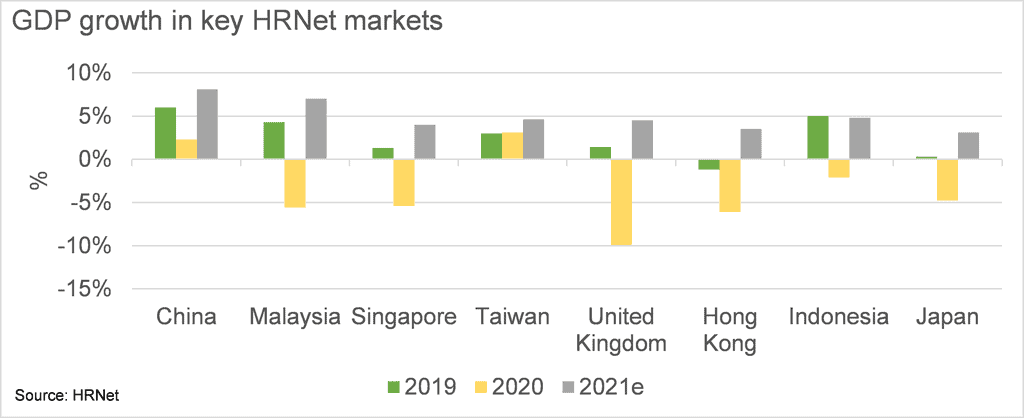

“Antifragile” as defined by Nassim Taleb refers to something which gets stronger during disorder. I think HRNet almost fits this description so I bought more HRNet shares after the company reported surprisingly resilient 2020 results. Healthy flexible staffing business resulted in revenue growing 2% and recurring net profit falling 4% during 2020 while operating cash flow grew 76%. With its resilient business model, I think HRNet is a cheap and safe way to bet on a V-shaped economic recovery in 2021 and secular growth in Asia.

HRNet is a Singapore-based staffing company with high returns on capital and a cheap valuation. Staffing and recruitment is a tough business but HRNet is laser-focused on profit margins with ROA averaging 12% respectively over 2018-20 and cheap with the company trading at only 3.8x trailing EV/EBITDA while net cash makes up 57% of its market capitalization.

Why is HRNet undervalued?

Small cap stock: SGD586 million market cap...