Will be a short post as there is only 1 million public shares available for application.

As such the allocation could be a disaster (similar to Econ Healthcare)

Pros

1) Good Revenue Growth that is driven by gain in profits.

Being a food manufactuer company, improving margins is important. As such, the company has done well improving its margins from 2019 to 2020. This has further improved in 1H 2021. As such, if the company does sustain its growth, it does not look expensive at all given a forward IPO PE of around 7.5 not accounting IPO Expenses.

2) Malaysia Growth Segment and Incentive to Manager is via profits.

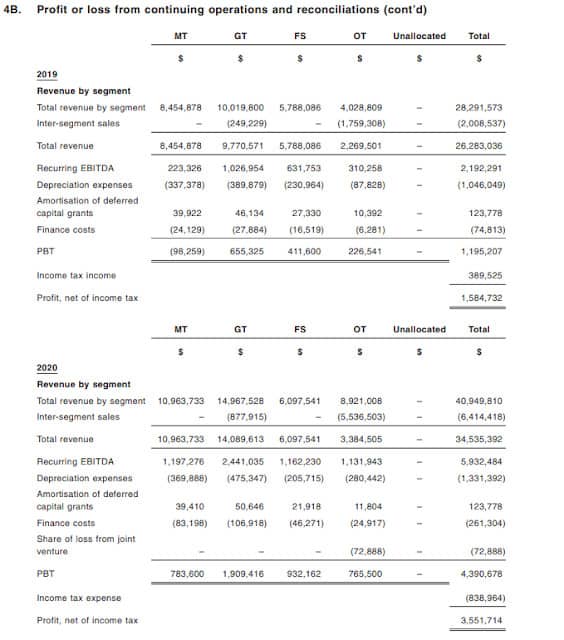

Looking at the revenue segment by country, one can identify quickly that the expansion in Malaysia is the reason for the growth in profits.

From 1.4m in 2018 to 2.3m in 2019 to 7.4m in 2020, this growth trajectory itself...