Source: Sunright Limited Corporate Website

After burn-in, a semiconductor device is tested to determine if it operates as intended. At the same time, the device is graded for its quality by testing the electrical characteristics and determining if it is operating within specified limits and functions.

Source: Sunright Limited Corporate Website

After burn-in, a semiconductor device is tested to determine if it operates as intended. At the same time, the device is graded for its quality by testing the electrical characteristics and determining if it is operating within specified limits and functions.

Source: Sunright Limited Corporate Website

Overall, both processes are critical within the production process of semiconductors.

Beyond the company’s production capabilities, this stock warrants a second look for investors, and we will unveil them layer by layer.

Latest result signals resilient in their business

Source: Sunright Limited Corporate Website

Overall, both processes are critical within the production process of semiconductors.

Beyond the company’s production capabilities, this stock warrants a second look for investors, and we will unveil them layer by layer.

Latest result signals resilient in their business

Source: Sunright 1H FY2021 Result Press Release

For 1H FY2021, Sunright’s revenue declined slightly by 3% year-on-year to S$58.69 million. Mr. Samuel Lim, Executive Chairman & Chief Executive Officer explained, “In the first six months of this financial year, we saw strong design wins with higher loadings for computing businesses. Consequently, the additional volume compensated for the lower loadings from our customers in the automotive sector.”

Despite the lower revenue, net profit attributable to Owners of the Company surged by more than 400% year-on-year to S$1.28 million. This can be seen from the lower employee benefits expense and depreciation of property, plant, and equipment.

In terms of outlook, Mr. Lim highlighted, “The on-going remote working environment and distance learning drove demands for personal computers, laptops, tablets, as a result of the global COVID pandemic.”

“We are seeing a continuing flow in demands from 5G, A.I. and iCloud markets. With the coronavirus pandemic in better control as vaccination programs are rolling out, our products and services should benefit under more stable market conditions.”

Interest alignment with investors and management

Source: Sunright 1H FY2021 Result Press Release

For 1H FY2021, Sunright’s revenue declined slightly by 3% year-on-year to S$58.69 million. Mr. Samuel Lim, Executive Chairman & Chief Executive Officer explained, “In the first six months of this financial year, we saw strong design wins with higher loadings for computing businesses. Consequently, the additional volume compensated for the lower loadings from our customers in the automotive sector.”

Despite the lower revenue, net profit attributable to Owners of the Company surged by more than 400% year-on-year to S$1.28 million. This can be seen from the lower employee benefits expense and depreciation of property, plant, and equipment.

In terms of outlook, Mr. Lim highlighted, “The on-going remote working environment and distance learning drove demands for personal computers, laptops, tablets, as a result of the global COVID pandemic.”

“We are seeing a continuing flow in demands from 5G, A.I. and iCloud markets. With the coronavirus pandemic in better control as vaccination programs are rolling out, our products and services should benefit under more stable market conditions.”

Interest alignment with investors and management

Source: ShareInvestor WebPro

The single largest shareholder for Sunright is Mr. Samuel Lim Syn Soo, holding a 54.93% stake. As the co-founder of the company, he currently also holds the position of Executive Chairman & Chief Executive Officer.

With his strong background of 45 years in the semiconductor industry, coupled with his stake in the company, investors can be assured that he has the capabilities, knowledge, and interest to ensure that the company is well positioned for growth.

Net Cash Position Across the Years

Source: ShareInvestor WebPro

The single largest shareholder for Sunright is Mr. Samuel Lim Syn Soo, holding a 54.93% stake. As the co-founder of the company, he currently also holds the position of Executive Chairman & Chief Executive Officer.

With his strong background of 45 years in the semiconductor industry, coupled with his stake in the company, investors can be assured that he has the capabilities, knowledge, and interest to ensure that the company is well positioned for growth.

Net Cash Position Across the Years

Source: ShareInvestor WebPro

Sunright has been in a net cash position over the years. Even so, its total debt to equity has been generally on a declining trend to just 0.17 times in FY2020. This is a good sign as it proves that Sunright is not heavily leveraged.

To further expand our dive into its financial health, Sunright’s liquidity ratios reflects that the company is financially stable, given the high current ratio and in particular, cash ratio. The ratio for FY2020 stood at 1.40 times, which indicates that its cash on hand exceeds its total current liabilities.

To give a sense of comparison, Avi-Tech Electronics Limited (SGX: BKY), the closest competitor of Sunright, is trading at S$0.39, with a cash ratio of 2.58 times and current ratio of 7.65 times.

Quick Analysis on the Implied Value of Sunright

Source: ShareInvestor WebPro

Sunright has been in a net cash position over the years. Even so, its total debt to equity has been generally on a declining trend to just 0.17 times in FY2020. This is a good sign as it proves that Sunright is not heavily leveraged.

To further expand our dive into its financial health, Sunright’s liquidity ratios reflects that the company is financially stable, given the high current ratio and in particular, cash ratio. The ratio for FY2020 stood at 1.40 times, which indicates that its cash on hand exceeds its total current liabilities.

To give a sense of comparison, Avi-Tech Electronics Limited (SGX: BKY), the closest competitor of Sunright, is trading at S$0.39, with a cash ratio of 2.58 times and current ratio of 7.65 times.

Quick Analysis on the Implied Value of Sunright

Source: Sunright 1H FY2021 Result Announcement

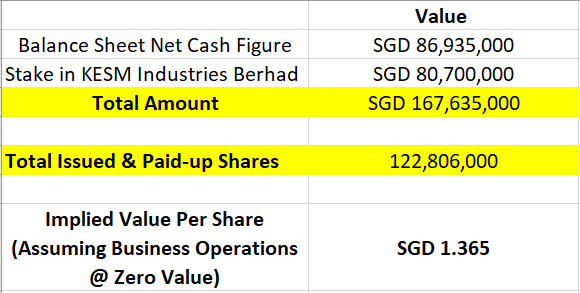

Based on the latest figure for 1H FY2021, Sunright has S$99.21 million worth of cash and short-term deposits in its balance sheet. If we offset its total loan and borrowings, its net cash amount would be S$86.93 million.

This amount alone is significantly higher than its current market capitalisation of S$55.87 million and it implies that investors are investing in the company at a discount to its net cash amount on hand, and its business operations for free.

Crown Jewel Asset – KESM Industries Berhad (9344.MY)

Source: Sunright 1H FY2021 Result Announcement

Based on the latest figure for 1H FY2021, Sunright has S$99.21 million worth of cash and short-term deposits in its balance sheet. If we offset its total loan and borrowings, its net cash amount would be S$86.93 million.

This amount alone is significantly higher than its current market capitalisation of S$55.87 million and it implies that investors are investing in the company at a discount to its net cash amount on hand, and its business operations for free.

Crown Jewel Asset – KESM Industries Berhad (9344.MY)

Sunright holds a 48.4% stake in Malaysia listed firm – KESM Industries Berhad (“KESM”).

Based on the current market price, its stake is worth around RM250.73 million (S$80.70 million) and this amount exceeds the entire market value of Sunright.

Sunright holds a 48.4% stake in Malaysia listed firm – KESM Industries Berhad (“KESM”).

Based on the current market price, its stake is worth around RM250.73 million (S$80.70 million) and this amount exceeds the entire market value of Sunright.

Source: ShareInvestor WebPro

KESM is the largest independent provider of burn-in, testing and electronic manufacturing services in Malaysia.

If we add up its net cash amount, the stake in KESM and assuming its business at zero value, the implied value of Sunright should be around S$1.36.

Here’s the calculations:

Source: ShareInvestor WebPro

KESM is the largest independent provider of burn-in, testing and electronic manufacturing services in Malaysia.

If we add up its net cash amount, the stake in KESM and assuming its business at zero value, the implied value of Sunright should be around S$1.36.

Here’s the calculations:

Sizeable Market Size for Sunright

According to a report by Transparency Market Research, the market size for the global wafer-level test and burn-in (“WLTBI”) market is estimated to exceed US$5.6 billion by 2031, expanding at a compound annual growth rate (“CAGR”) of around 4%.

The growth in the WLTBI market can be attributed to the increasing usage of semiconductors in both Automotive and Telecom sectors:

Sizeable Market Size for Sunright

According to a report by Transparency Market Research, the market size for the global wafer-level test and burn-in (“WLTBI”) market is estimated to exceed US$5.6 billion by 2031, expanding at a compound annual growth rate (“CAGR”) of around 4%.

The growth in the WLTBI market can be attributed to the increasing usage of semiconductors in both Automotive and Telecom sectors:

- Increased adoption of electronic systems and parts in automobiles are creating more demand for semiconductor.

- Increased adoption of silicon photonics devices for data centers and 5G infrastructure, fiber optic transceivers, and mobile communication systems.

This is a sponsored post.