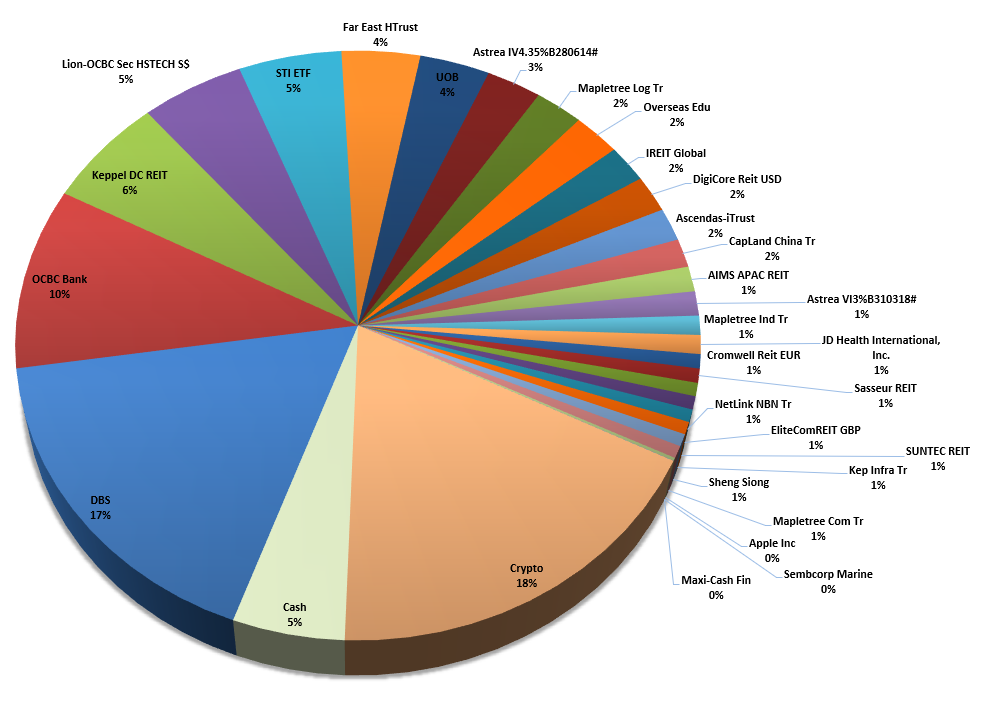

My Lazy Man Portfolio - excluding Robo and CPF[/caption]

[caption id="attachment_1512974" align="aligncenter" width="1079"]

My Lazy Man Portfolio - excluding Robo and CPF[/caption]

[caption id="attachment_1512974" align="aligncenter" width="1079"] My Lazy Man Portfolio - including Robo and CPF[/caption]

My Lazy Man Portfolio - including Robo and CPF[/caption]

My Little One (MoneyOwl)

Start Date: May 2020

Allocation: 60% Equities, 40% Fixed Income

Investment Amount: $300 per month

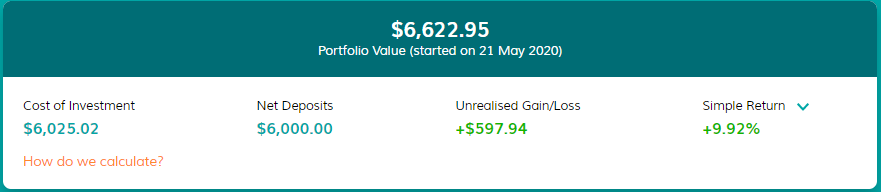

My Sweetheart and I (Endowus)

Start Date: May 2020

Allocation: 60% Equities, 40% Fixed Income

Investment Amount: $300 per month

My Sweetheart and I (Endowus)

Start Date: Jun 2020

Allocation: 60% Equities, 40% Bonds

Investment Amount: $300 per month

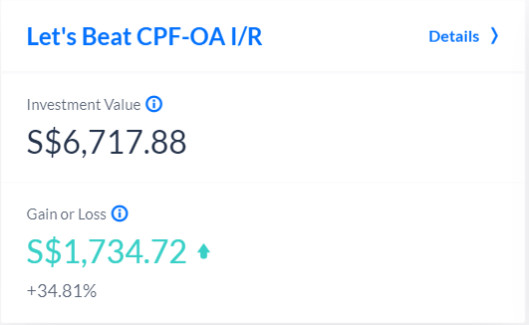

Let’s Beat CPF (Endowus)

Start Date: Jun 2020

Allocation: 60% Equities, 40% Bonds

Investment Amount: $300 per month

Let’s Beat CPF (Endowus)

Start Date: Jun 2020

Allocation: 80% Equities, 20% Bonds

Investment Amount: $5,000 lump sum from CPF-OA

Start Date: Jun 2020

Allocation: 80% Equities, 20% Bonds

Investment Amount: $5,000 lump sum from CPF-OA

For the year ahead, I will be building up cash while focusing on adding into more dividend stocks that I already own. The only new stock that I will buy will be related to the Metaverse or NFT. Stocks

- Only look to add into existing stocks only

- Load stocks with > 5% forward dividend -

since banks has a positive correlation with Crypto, if forward dividend is almost similar, I will prioritize REITS over Banks.On second thoughts, since REITS have been issuing rights, I will prioritize Banks instead. - Buy Metaverse Stock/ETF

- Portfolio rule of no more than 20% for a single stock still apply - Stocks and Crypto only – exclude Robo and CPF investments

- Stop buying any more China Tech because of my portfolio rule and there are no dividends.

- Dividend Stocks to make up at least 50% of the portfolio – I am looking at Cash dividends only, hence Crypto Farming/Yielding is excluded.

- Fairly early adopter with a reasonable margin of safety but unlikely to pump in any new cash. Cash will be channeled into stocks instead.

- Will recycle the coins that I already have with a combination of Farming and Staking.

- Farm using different type of Liquidity Pools

- Explore Correlation

- Buy another USD 500 of Cardona (ADA) to participate in SUNDASWAP ICO

- Balance of approximately SGD 500 in Fiat wallet

- Work towards achieving SGD 5,000 of CRO by Jun 2022 so that I can upgrade from Ruby to Indigo.

- Explore the use of a Crypto Portfolio Tracker - https://coinstats.app/

- Explore Portfolio Management of 50% in BTC/ETH, 25% Stablecoins and 25% Altcoins

- Changing from HDB to Bank loan.

- Retirement Sum Topping-Up Scheme (RSTU) – by May 2022

I’m just thinking it this way. First, on a personal basis - both of you are still young and working. Your savings in the next 20 years will probably be more than whatever amount you decide to invest now. Second, on a practical basis - it’s not easy to find a 100% capital guaranteed 2% returns now. Even if you do, your real returns after inflation may be ~0% or (likely) less. Third, on portfolio management - in HK and SG etfs, you are looking at a total of >50 companies across various industries (though there may be slightly more in property and banks currently but may change for the better). Hk has a little more China exposure while Sg has a little more ASEAN exposure. There could be some growth there if we are lucky. This kind of diversification, is probably safer than any ‘capital guarantee’ provided by any non-Sg govt institutions in my opinion. Fourth, let’s look at our possible downside: If hk and Sg companies are so hopeless that their prices are exactly the same 20 years later (zero appreciation) and if they just manage to maintain their payout, dividend yields will be 2.5-3%. If you reinvest them every year, you are already compounding the money at 2.5-3%. That alone should meet your goal of 2% despite having zero appreciation. If let’s say it’s so useless that all companies somehow died and there’s no new companies replacing the index (extremely unlikely), it’s only up to $300K. (I mentioned just now anything above maybe $300K put in things like ssb). Fifth, what’s the upside? Let’s say we get 2.8% yield and 3.2% growth for 6% compounding. $100K investment 20 years later will be $320K. What you saved from working maybe 15 years previously will be worth 48 years of savings 20 years later. I’m pretty sure despite being stagnant in recent years, sti and hsi long term appreciation should be easily 3-4% before dividends. These are my explanations and rationale to your wife and you. Not forcing your wife or you but it’s a genuine suggestion.Blog Revamp

- New revamp site to launch in Feb 2022

- Aggregate Videos

- Affiliate Links – to derivatives that I personally use

- Google Digital Garage – Fundamentals of Digital Garage

- Domain forwarding thefinance.finance

- Blockchain domain

Featured Photo by Executium on Unsplash