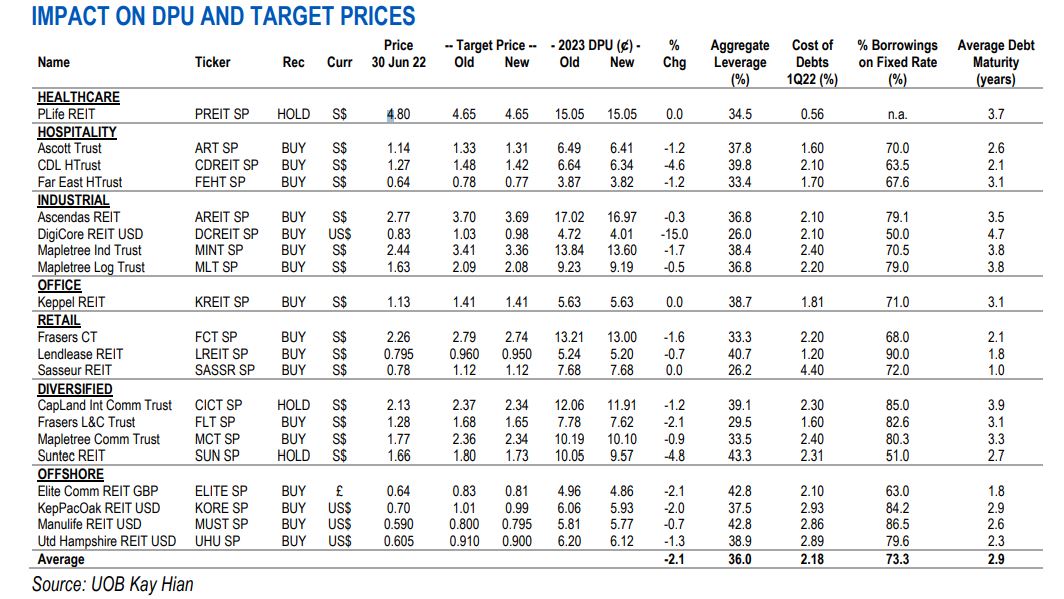

Excerpts from UOBKayHian report The rapid surge in interest rates affects Singapore Reits (S-REITs) who have not adequately hedged their cost of borrowings. We cut DCREIT’s 2023 DPU by 15% but upgrade the S-REIT to BUY after the recent 35% sell-off. MLT has only 11% of its borrowings exposed to rising interest rates. Stay invested in hospitality, retail and office REITs as reopening plays. BUY ART (Target: S$1.31), FCT (Target: S$2.74), FEHT (Target: S$0.77) and LREIT (Target: S$0.95). Maintain OVERWEIGHT.