Eight and a half years ago, I came across some articles on that changed the way I look at retirement spending.

It was also the time when many of us started hearing about the 4% safe withdrawal rate. And thus I got curious whether we can spend 4% of the wealth accumulated conservatively, and then consistently increase the spending based on inflation.

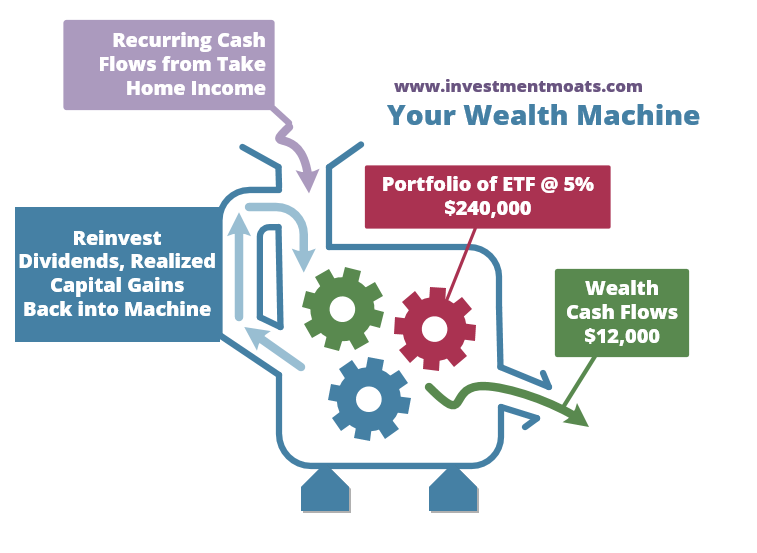

So if my expenses is $2000/mth or $24,000/yr, I would need to accumulate $24,000 / 0.04 = $600,000.

After investing for some time, I realize in our region we can get a lot of dividend stocks conservatively yielding at least 5% in dividend income. If you factor in at least some inflation-adjusted growth, these stocks can give a total return of 7%, if not more.

So why can’t I use a 5% withdrawal rate?

In that way, I would just need to accumulate $24,000/0.05 = $480,000.

My target for financial freedom seemed so much closer!...