Today’s article is a continuation of my personal notes series, where I will share some honest takes on how I frame some personal financial decision-making.

Recently, I decided to tackle some of my future healthcare considerations.

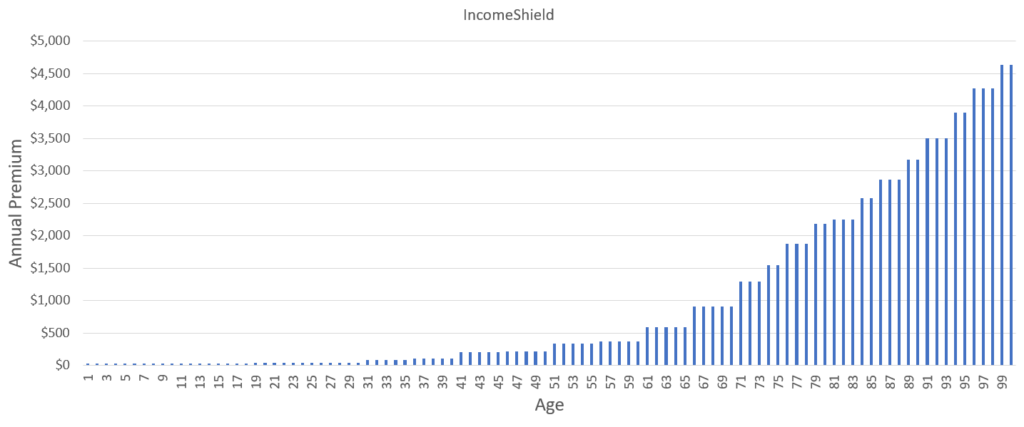

In cutting my F.I. capital needs for insurance premiums from $131,366 to $58,132, I explain that a large part of our insurance premiums do not adjust based on inflation and can be rather fixed. This means that adding our insurance premium needs to a whole retirement income figure is not very optimal.

In my calculation, I decided to leave out how much to set aside for health insurance premiums.

Health insurance is commonly known as Medishield LIFE and the private integrated shield plans and their riders are provided by Singlife, Income Insurance, AIA, Prudential, Great Eastern, HSBC and Raffles Insurance.

In this article, I will explain why I decide to set aside $80,000 of my current CPF Ordinary Savings monies to fund my future health insurance premiums....