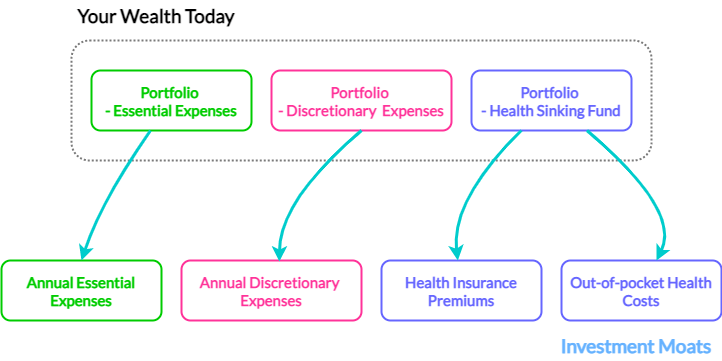

In my last article, I look at whether we can create a health sinking fund to pre-fund our health and wellness expenses in financial independence. When we do not have income coming in, and we do not know whether we will be able to accumulate again, how much should be inside a health sinking fund? How conservative or less conservative should it be? The first article focus only on one area where we need funding: Funding our health insurance plans, which is more commonly known as our shield plans. We learn that the nature of cash flow needed in health insurance is unique in that the premiums are low when we are younger, very expensive when we are older, and that this premium schedule does not stay constant. If we lump our health insurance expense needs together with our other consumption needs, it will be tough to model. If...

{kind=link}