In the latest financial result, KORE announced the surprise of suspension in dividends. The REIT elaborated it had considered other avenues such as fund raising and sale of building, but they were not beneficial to Unitholders. While the REIT is rational, I feel the REIT is being too cautious with its cashflow.

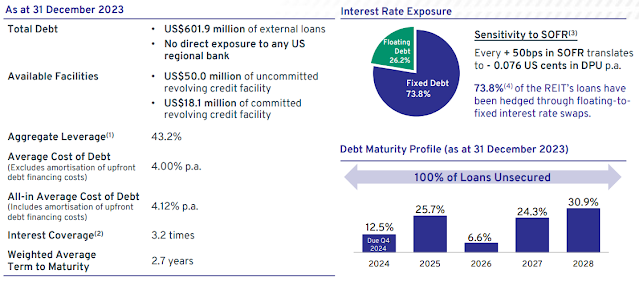

Debt Profile

KORE has US$78 mil of debt due in 4Q2024. With a cash generation ability of US$77 mil, expected CAPEX of US$30mil and cash balance of $43.7 mil, KORE is too cautious with expectations it is unable to refinance its tranche due in 4Q2024. With its cash flow and cash balance, KORE can repay in full without going to the bank.

KORE Cashflow is US$77 Mil per year

Effects of Full Repayment

Assuming a full repayment of US$70 mil at end 2024, KORE leverage will fall to 38.2% (barring further valuation fall). This I feel shows KORE is too cautious. It could have paid out a bit of...