I took a quick glance at the draft IPO prospectus.

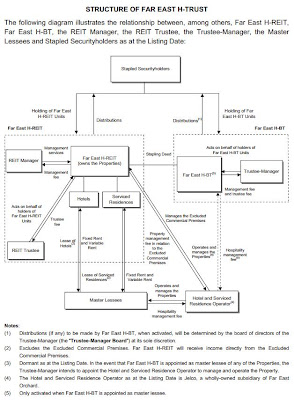

Just the structure alone, its is much better than the Ascendas Hospitality Trust where all the hotels are parked under the Hotel Reit and not under the business trust.

According to the email, the price will range from 86c (6% annualised yield) and 93c (6.5% annualised yield) for FY 12E.

The presence of reputable cornerstone investors are also very reassuring and it will be them who will dictate the pricing.

CDL H-Trust is trading at 5.7% yield and Ascott Residence Trust is trading at 7.2% yield. In this regard, my only complaint is that the yields are on the 'low side'. It will be good if Far East can leave some meat on the table by pricing the issue at the mid to lower end of 86 cents. If it prices it at 93c, i am afraid ......

According to the email, the price will range from 86c (6% annualised yield) and 93c (6.5% annualised yield) for FY 12E.

The presence of reputable cornerstone investors are also very reassuring and it will be them who will dictate the pricing.

CDL H-Trust is trading at 5.7% yield and Ascott Residence Trust is trading at 7.2% yield. In this regard, my only complaint is that the yields are on the 'low side'. It will be good if Far East can leave some meat on the table by pricing the issue at the mid to lower end of 86 cents. If it prices it at 93c, i am afraid ......