[caption id="attachment_1911" align="alignright" width="233" caption="Trendspotting - Residential Price Index"]

[/caption]

I was thinking which of my blogs I should put this article in and decided that the Trendspotting one is the most appropriate although the article is not highlighting a trend to buy into; rather it is advising against buying into something. Besides, I haven't written in Trendspotting for some time already.

There has been pessimism over the property market since mid-2008, and justifiably in my view, given the potential looming supply of private homes coming onstream over 2009-10. However, recently there appears to be a wellspring of renewed optimism in the market, magnified through the press, over the successful launches of several mass-market developments, notably Caspian in Jurong East and Alexis in Alexandra. I also notice threads appearing online trumpeting the recovery of the housing market. And of course, you hear again the boss of one of our local big developers declaring his (perrenially) optimistic views about the property market during the company's results release.

In my opinion this is false optimism tinged with acute conflict of interest from the various parties involved. Let's get the overall feel of things:

1) One of the key failures in the current global market is liquidity shortage leading to tight credit across the board. The logical thing is to expect demand for big-ticket items that require loan financing to be in the first line of fire from a credit crunch. That is why auto companies across the world are seeing an unbelievable slump in demand over the last 2-3 months, especially when they are considered discretionary items as well. In the US, without government assistance (eg. loan restructuring), things would have been worse in their real estate industry. In Singapore, I have heard people claiming that low SIBOR rates (benchmarks for home loans) are evidence that liquidity is available and cheap. This is not true if firstly, the banks are more stringent in their screening process on who to lend to, and secondly if the premium over SIBOR (typically home loans are quoted at SIBOR + premium) are increased accordingly as SIBOR is reduced. I understand both are happening. Really..... if I were a banker, would I be lending like normal times, and at lower rates than normal to loan seekers now? Get real!

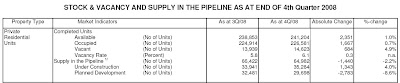

2) The supply-demand dynamics just doesn't look exciting. Why would anyone want to buy now why there is a large supply overhang. Let's look at some numbers from URA, the voice of reason (statistics don't lie):

Click on the picture to make it larger. Basically, the figure as of 4Q08 show that currently total available/completed private residential units number about 230,000-240,000 (mostly occupied of course). The supply in the pipeline is about 66,000, half of which are under construction and the other half being planned. Think about it: there is looming supply amounting to one-quarter of Singapore's existing private housing stock, the latter of which was built up over decades. That means massive demand has to come in to absorb this supply overhang, and that demand must amount to say, one-quarter of Singapore's mid-to-upper middle-class (that can afford condos). Are we expecting 25% increase in this population over say, 4-5 years? Of course, there're the cash-rich enblocers, but common sense tells me they can't amount to that many; besides they'll likely want to tighten belts too.

The only reason for people to buy in the face of such an obvious supply overhang, whether for personal dwelling or for investment purposes, will be if prices drop to a sufficiently attractive level..... which brings us to our third point.

3) Price levels are not that attractive. You only have to look at the URA Residential Price Index to make that conclusion:

Read more...

[/caption]

I was thinking which of my blogs I should put this article in and decided that the Trendspotting one is the most appropriate although the article is not highlighting a trend to buy into; rather it is advising against buying into something. Besides, I haven't written in Trendspotting for some time already.

There has been pessimism over the property market since mid-2008, and justifiably in my view, given the potential looming supply of private homes coming onstream over 2009-10. However, recently there appears to be a wellspring of renewed optimism in the market, magnified through the press, over the successful launches of several mass-market developments, notably Caspian in Jurong East and Alexis in Alexandra. I also notice threads appearing online trumpeting the recovery of the housing market. And of course, you hear again the boss of one of our local big developers declaring his (perrenially) optimistic views about the property market during the company's results release.

In my opinion this is false optimism tinged with acute conflict of interest from the various parties involved. Let's get the overall feel of things:

1) One of the key failures in the current global market is liquidity shortage leading to tight credit across the board. The logical thing is to expect demand for big-ticket items that require loan financing to be in the first line of fire from a credit crunch. That is why auto companies across the world are seeing an unbelievable slump in demand over the last 2-3 months, especially when they are considered discretionary items as well. In the US, without government assistance (eg. loan restructuring), things would have been worse in their real estate industry. In Singapore, I have heard people claiming that low SIBOR rates (benchmarks for home loans) are evidence that liquidity is available and cheap. This is not true if firstly, the banks are more stringent in their screening process on who to lend to, and secondly if the premium over SIBOR (typically home loans are quoted at SIBOR + premium) are increased accordingly as SIBOR is reduced. I understand both are happening. Really..... if I were a banker, would I be lending like normal times, and at lower rates than normal to loan seekers now? Get real!

2) The supply-demand dynamics just doesn't look exciting. Why would anyone want to buy now why there is a large supply overhang. Let's look at some numbers from URA, the voice of reason (statistics don't lie):

[/caption]

I was thinking which of my blogs I should put this article in and decided that the Trendspotting one is the most appropriate although the article is not highlighting a trend to buy into; rather it is advising against buying into something. Besides, I haven't written in Trendspotting for some time already.

There has been pessimism over the property market since mid-2008, and justifiably in my view, given the potential looming supply of private homes coming onstream over 2009-10. However, recently there appears to be a wellspring of renewed optimism in the market, magnified through the press, over the successful launches of several mass-market developments, notably Caspian in Jurong East and Alexis in Alexandra. I also notice threads appearing online trumpeting the recovery of the housing market. And of course, you hear again the boss of one of our local big developers declaring his (perrenially) optimistic views about the property market during the company's results release.

In my opinion this is false optimism tinged with acute conflict of interest from the various parties involved. Let's get the overall feel of things:

1) One of the key failures in the current global market is liquidity shortage leading to tight credit across the board. The logical thing is to expect demand for big-ticket items that require loan financing to be in the first line of fire from a credit crunch. That is why auto companies across the world are seeing an unbelievable slump in demand over the last 2-3 months, especially when they are considered discretionary items as well. In the US, without government assistance (eg. loan restructuring), things would have been worse in their real estate industry. In Singapore, I have heard people claiming that low SIBOR rates (benchmarks for home loans) are evidence that liquidity is available and cheap. This is not true if firstly, the banks are more stringent in their screening process on who to lend to, and secondly if the premium over SIBOR (typically home loans are quoted at SIBOR + premium) are increased accordingly as SIBOR is reduced. I understand both are happening. Really..... if I were a banker, would I be lending like normal times, and at lower rates than normal to loan seekers now? Get real!

2) The supply-demand dynamics just doesn't look exciting. Why would anyone want to buy now why there is a large supply overhang. Let's look at some numbers from URA, the voice of reason (statistics don't lie):

Click on the picture to make it larger. Basically, the figure as of 4Q08 show that currently total available/completed private residential units number about 230,000-240,000 (mostly occupied of course). The supply in the pipeline is about 66,000, half of which are under construction and the other half being planned. Think about it: there is looming supply amounting to one-quarter of Singapore's existing private housing stock, the latter of which was built up over decades. That means massive demand has to come in to absorb this supply overhang, and that demand must amount to say, one-quarter of Singapore's mid-to-upper middle-class (that can afford condos). Are we expecting 25% increase in this population over say, 4-5 years? Of course, there're the cash-rich enblocers, but common sense tells me they can't amount to that many; besides they'll likely want to tighten belts too.

The only reason for people to buy in the face of such an obvious supply overhang, whether for personal dwelling or for investment purposes, will be if prices drop to a sufficiently attractive level..... which brings us to our third point.

3) Price levels are not that attractive. You only have to look at the URA Residential Price Index to make that conclusion: Read more...

Click on the picture to make it larger. Basically, the figure as of 4Q08 show that currently total available/completed private residential units number about 230,000-240,000 (mostly occupied of course). The supply in the pipeline is about 66,000, half of which are under construction and the other half being planned. Think about it: there is looming supply amounting to one-quarter of Singapore's existing private housing stock, the latter of which was built up over decades. That means massive demand has to come in to absorb this supply overhang, and that demand must amount to say, one-quarter of Singapore's mid-to-upper middle-class (that can afford condos). Are we expecting 25% increase in this population over say, 4-5 years? Of course, there're the cash-rich enblocers, but common sense tells me they can't amount to that many; besides they'll likely want to tighten belts too.

The only reason for people to buy in the face of such an obvious supply overhang, whether for personal dwelling or for investment purposes, will be if prices drop to a sufficiently attractive level..... which brings us to our third point.

3) Price levels are not that attractive. You only have to look at the URA Residential Price Index to make that conclusion: Read more...