This chapter focuses on designing political and economic institutions. I will shoehorn this chapter into a discussion about the relative strengths and weaknesses of our CPF system.

There are four aspects to such institutions.

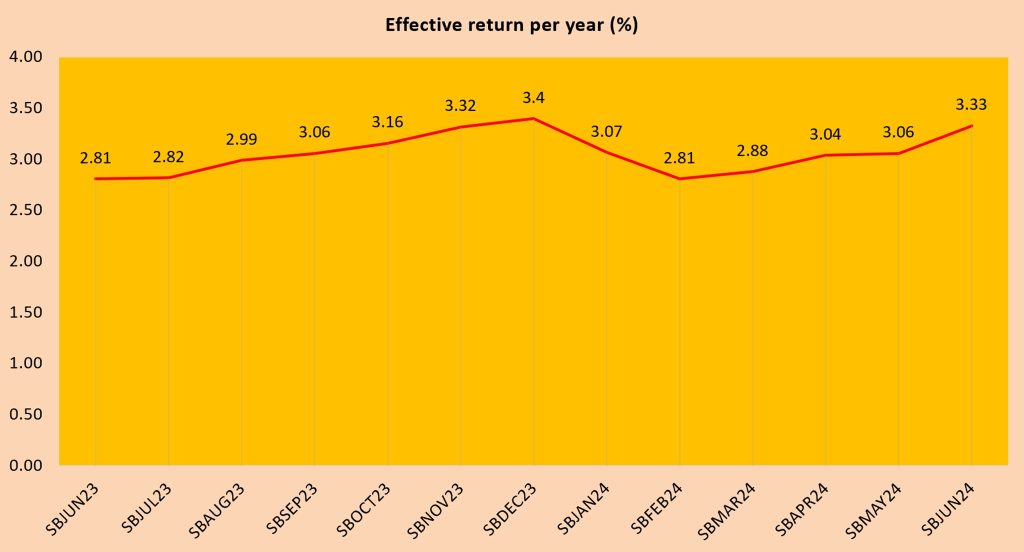

Information consists of what participants know and what should be revealed to them. All Singaporeans know what interest rates they should expect to receive for their CPF accounts. Singaporeans are probably less clear about what kind of payouts they expect to receive from CPF Life when they hit 65.

Incentives cover the costs and benefits of taking some actions. Contributing your money via the Retirement Sum Topping-Up scheme leads to tax deductions that can benefit folks in the higher income brackets more than those in the lower brackets.

Aggregation show how individual actions translate into collective outcomes. The collective outcome of CPF is that Singapore insures itself from the bad financial habits of other Singaporeans and have a tool to

...