Ah… the

CIMB FastSaver Account.

A favourite of many freelancers, the self-employed, couples looking to grow their money in a joint account.

And generally, people who want a

high-interest savings account that is

relatively fuss-free.

But alas…

COVID-19.

Economy bad.

Interest rate not good.

Yada yada yada.

You know the whole spiel by now…

PSA: there will be

changes made to the CIMB FastSaver Account come 15 July 2020.

TL;DR: Changes to CIMB FastSaver from 15 July 2020

| Requirements |

Before 15 July 2020 |

After 15 July 2020 |

Changes in 2020 |

| First $50,000 |

1.00% p.a. |

0.50% p.a. |

-0.50% p.a. |

| Next $25,000 |

1.50% p.a. |

0.80% p.a. |

-0.70% p.a. |

| Next $25,000 |

1.80% p.a. |

1.50% p.a. |

-0.30% p.a. |

| Above $100,000 |

0.60% p.a. |

0.40% p.a. |

-0.20% p.a. |

The CIMB FastSaver’s interest rates requirements are really straightforward.

There’s no:

- salary crediting

- bill payments

- credit card spend

- investment purchases

- monthly fees

It’s kinda like the

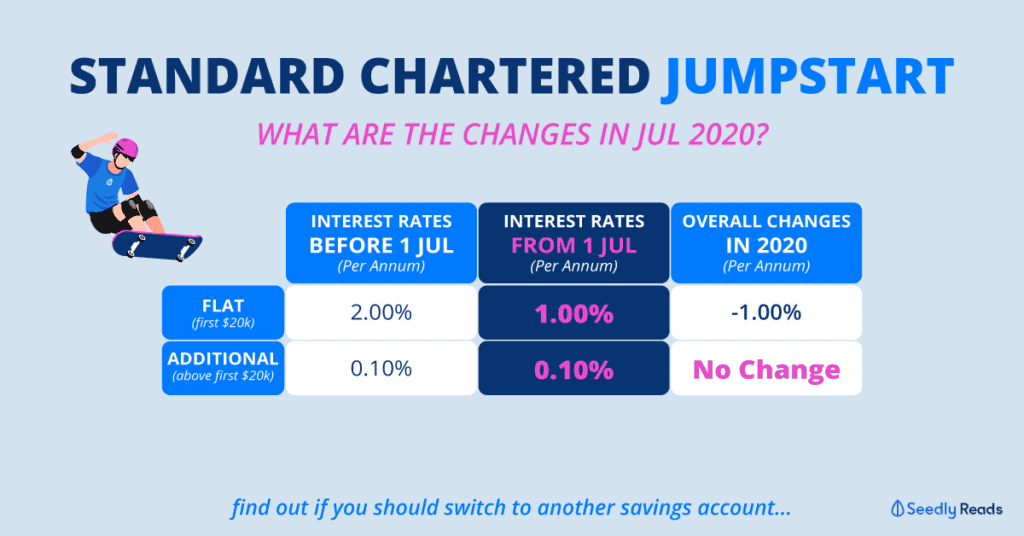

Standard Chartered JumpStart — which, unfortunately, also just revised its interest rates.

Just put your money in there and let it grow.

And just like the JumpStart, the FastSaver will also be slashing its interest rates too....