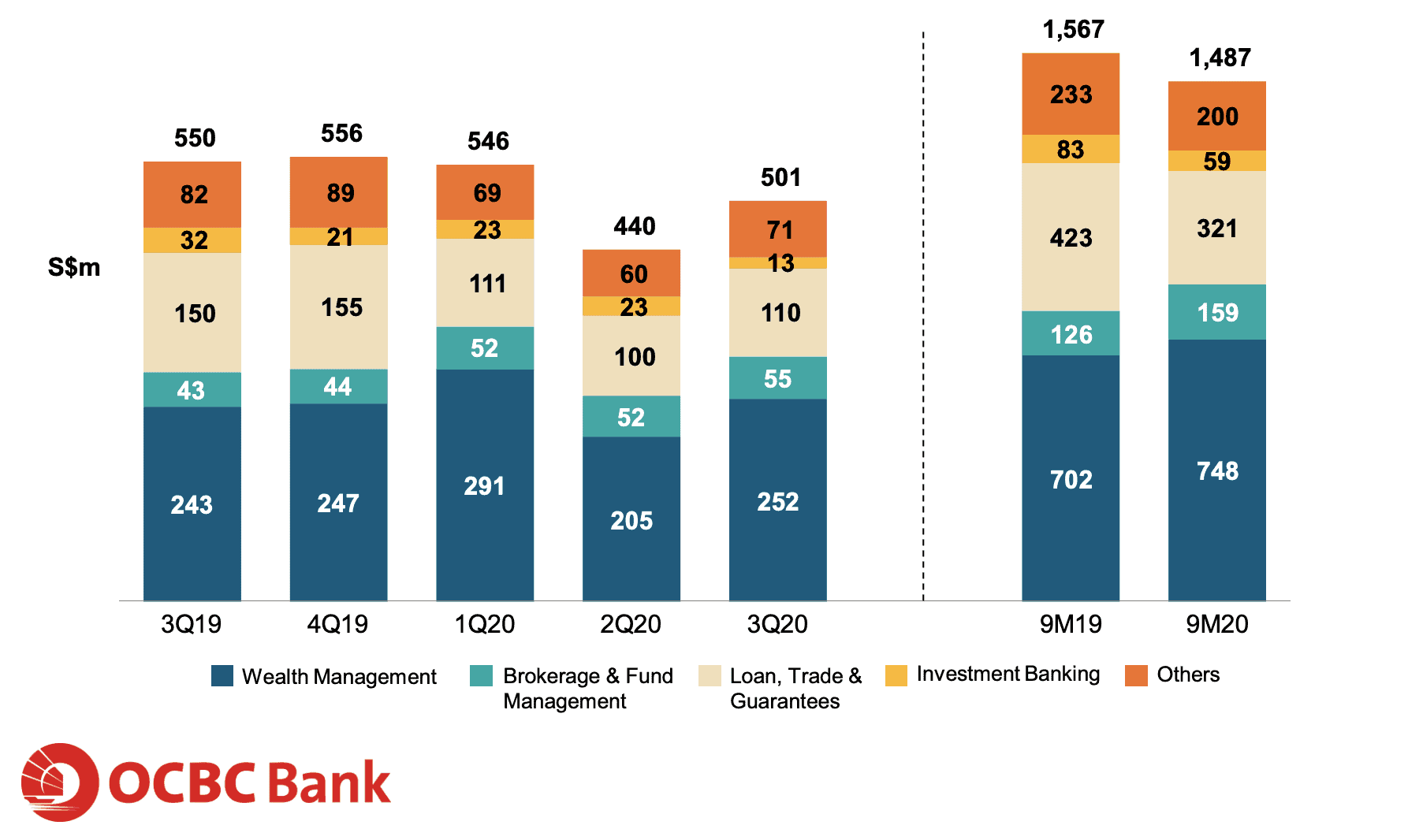

I understand that banks have been a lacklustre of late given the whole COVID-19 Pandemic and how there has been huge provisions for loan impairments/dividend cuts amongst our 3 local banks. However, having reviewed the recent 3Q earnings release by DBS and OCBC, I wanted to comment on an interesting point I noticed.

Looking at the below 2 snapshots, it shows the net fees & commissions for 3Q the respective banks have made from their ancillary services.

The interesting point would be on both banks’ wealth management services that is recording much higher growth rates of mid-20%. The low interest rate environment is something that is already a given and has been priced into current valuations. However, with this new wealth management segment, it will be able to offset the decline in net interest rate income for the banks.

The last time where Singapore Banks were facing a low interest rate environment, which was 2007/08 Global Financial Crisis...