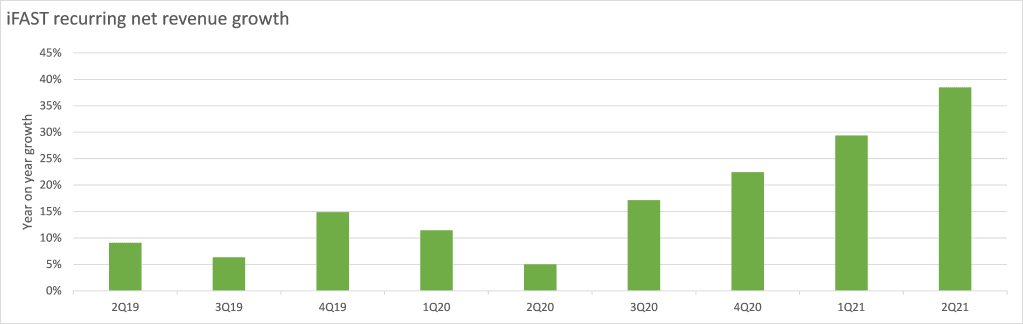

iFAST second 2021 results were decent but not good enough for the company’s high valuation. Most of the company’s key metrics including net revenue and profit were up year on year but down quarter on quarter because of lower stockbroking commissions. This sequential decline in net profit broke the company’s winning streak where net profit grew sequentially for 9 consecutive quarters.

TLDR summary: I’m a bit disappointed but I’ll be looking to add more shares on weakness. iFAST is making all the right moves to be a regional wealth management Fintech (eg. cutting fees, adding stockbroking services, digital banking license bid, Hong Kong MPF contract). iFAST is in the right place at the right time. This quarter is just a speed bump in their compounding journey.

From iFAST

“The Group’s assets under administration (“AUA”) continued to register new record levels, reaching S$17.54 billion as at 30 June 2021, a growth of 57.3% YoY and 21.4% YTD. The AUA of unit trusts,...