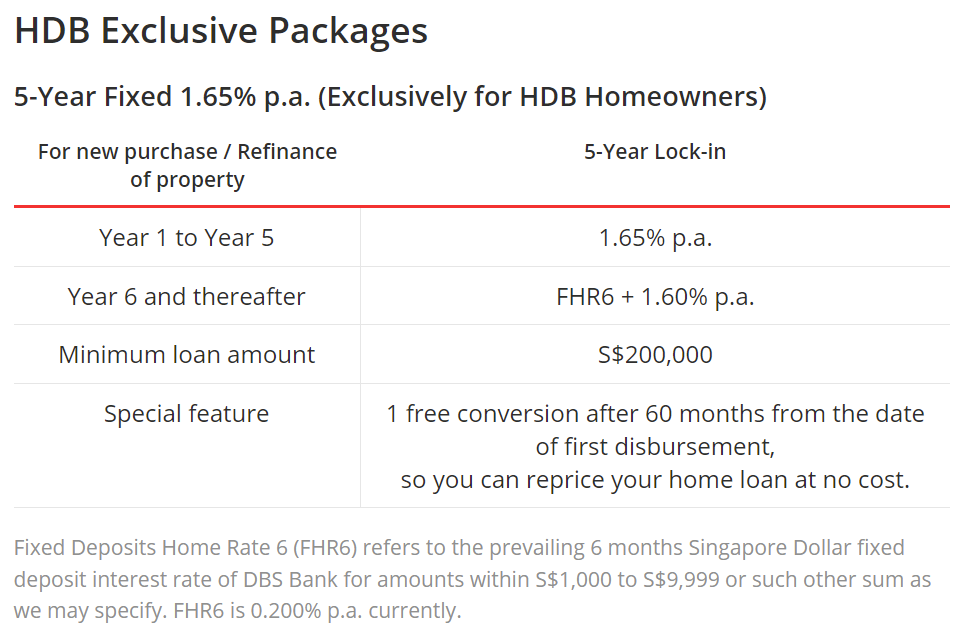

One of the biggest reason why I like HDB loan is the Interest Rate certainty. Granted 2.6% is not exactly competitive but at least I know it is unlikely to increase and will not impact my cash flow. Hence having a fix 1.65% for 5 years is very appealing (it was 1.55% just a month ago - talk about procrastinating).

One of the biggest reason why I like HDB loan is the Interest Rate certainty. Granted 2.6% is not exactly competitive but at least I know it is unlikely to increase and will not impact my cash flow. Hence having a fix 1.65% for 5 years is very appealing (it was 1.55% just a month ago - talk about procrastinating).

Comparing my current HDB loan against DBS, I would have save $29,354 in interest over 19 years and 1 month or $13,300 in 5 years. The next question is what happens on the 6th year. Everyone has their own strategy and here is mine.

At the end of the 5th year, my loan amount will be $284,421.66 - (12 months x 5 yrs x $1,449) = $284,421.66 - $86,400 = $198,021.66. I am pretty certain if my loan amount is less than $200,000, no banks will be willing to take me in since there is not much money to be made, hence I am pretty much stuck with DBS. Interest rates then may remain the same, lower or more. I assume the worse case scenario where the interest rate is higher than HDB.

I currently have $39,000 in CPF-OA and base on a very conservative estimate, I should be able grow my CPF-OA by $28,000 giving me a total of $67,000 in 5 years. If I were to use the entire amount to pay off my outstanding loan, I will still have to pay $198,021.66 - $67,000 = $131,921.66. I have not factor in any CPF contribution from bonus, pay increment, a reduce monthly payment and my wife's own CPF-OA. I am fairly confident that at the end of the 5th year, I can reduce the loan to less than $100,000 by exhausting both my wife and my CPF-OA. I am able to reduce the loan even further by half or $50,000 but utilizing my existing cash reserves, hence I will only need to service a outstanding loan of $50,000 at the end of the 5th year. This may not sound like a very wise move but this is assuming the worse case scenario where the bank interest rate become ridiculously high.

An added perk is my wife is a DBS Multiplier account and will get to enjoy a slightly higher interest rate.

The number one risk is that my wife and I lose our jobs or have a pay cut. After coming out from the pandemic, I am fairly confident that this will not happen in the next 5 years unless there is an event even worse than the pandemic - War, Alien Invasion, Super Virus, Rise of the machines (ok, I better stop my imagination).

Questions that I will be asking DBS:

FAQ

Q1: My strategy relies heavily on the special feature of "1 free conversion after 60 months from the date of first disbursement, so you can reprice your home loan at no cost." Are there any hidden cost for repricing and refinancing?

Q2: "Receive a S$2,000 Cash Reward when you refinance your home loan to us with a minimum loan amount of S$250,000." I now know that this cash reward is not entirely free as it is use to offset the fees e.g. Legal, valuation etc. Please provide the break-down of all the fees.

Q3: If I were to remain with DBS at the end of the 5th year, are there any restrictions to the reprice and loan period? Example, I cannot reduce the loan to less than $X amount say $100,000 and the minimum loan period must be at least Y years say 15 years.

Q4: Please provide the break-down of all the fees if I were to carry on with DBS after 5 years.

Q5: How will my wife get to benefit from the increase DBS Multiplier Interest Rate?

Comparing my current HDB loan against DBS, I would have save $29,354 in interest over 19 years and 1 month or $13,300 in 5 years. The next question is what happens on the 6th year. Everyone has their own strategy and here is mine.

At the end of the 5th year, my loan amount will be $284,421.66 - (12 months x 5 yrs x $1,449) = $284,421.66 - $86,400 = $198,021.66. I am pretty certain if my loan amount is less than $200,000, no banks will be willing to take me in since there is not much money to be made, hence I am pretty much stuck with DBS. Interest rates then may remain the same, lower or more. I assume the worse case scenario where the interest rate is higher than HDB.

I currently have $39,000 in CPF-OA and base on a very conservative estimate, I should be able grow my CPF-OA by $28,000 giving me a total of $67,000 in 5 years. If I were to use the entire amount to pay off my outstanding loan, I will still have to pay $198,021.66 - $67,000 = $131,921.66. I have not factor in any CPF contribution from bonus, pay increment, a reduce monthly payment and my wife's own CPF-OA. I am fairly confident that at the end of the 5th year, I can reduce the loan to less than $100,000 by exhausting both my wife and my CPF-OA. I am able to reduce the loan even further by half or $50,000 but utilizing my existing cash reserves, hence I will only need to service a outstanding loan of $50,000 at the end of the 5th year. This may not sound like a very wise move but this is assuming the worse case scenario where the bank interest rate become ridiculously high.

An added perk is my wife is a DBS Multiplier account and will get to enjoy a slightly higher interest rate.

The number one risk is that my wife and I lose our jobs or have a pay cut. After coming out from the pandemic, I am fairly confident that this will not happen in the next 5 years unless there is an event even worse than the pandemic - War, Alien Invasion, Super Virus, Rise of the machines (ok, I better stop my imagination).

Questions that I will be asking DBS:

FAQ

Q1: My strategy relies heavily on the special feature of "1 free conversion after 60 months from the date of first disbursement, so you can reprice your home loan at no cost." Are there any hidden cost for repricing and refinancing?

Q2: "Receive a S$2,000 Cash Reward when you refinance your home loan to us with a minimum loan amount of S$250,000." I now know that this cash reward is not entirely free as it is use to offset the fees e.g. Legal, valuation etc. Please provide the break-down of all the fees.

Q3: If I were to remain with DBS at the end of the 5th year, are there any restrictions to the reprice and loan period? Example, I cannot reduce the loan to less than $X amount say $100,000 and the minimum loan period must be at least Y years say 15 years.

Q4: Please provide the break-down of all the fees if I were to carry on with DBS after 5 years.

Q5: How will my wife get to benefit from the increase DBS Multiplier Interest Rate?

This is a developing post - I will visit it every year and definitely at the end of the 5th year or Dec 2026.