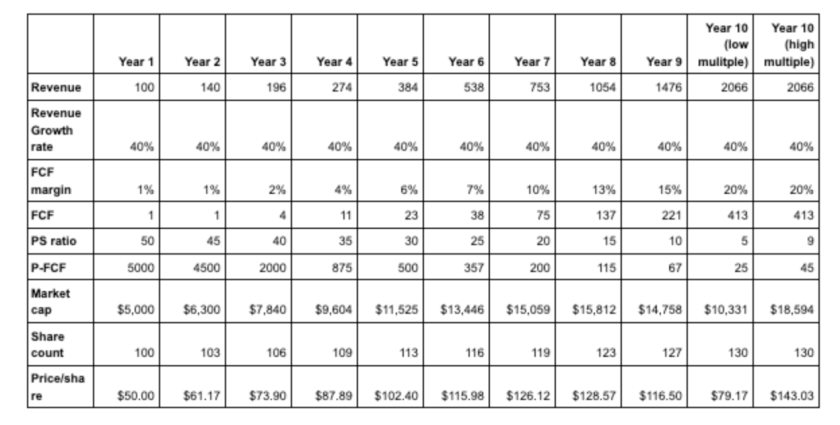

Investors who have had a vested interest in high-growth stocks in the past year, myself included, have (to put it mildly) experienced steep drawdowns. This begs the question, did we overpay for these companies? Many high-growth stocks in early 2021 were trading at high valuations and it was not uncommon to find such stocks trading at price-to-sales (P/S) multiples of more than 30. Their P/S multiples have since collapsed. Was that just too expensive or are multiples too cheap now? Mapping the future To answer this question, we need to make certain assumptions about the future. Let’s make the following conservative assumptions. First, in 10 years’ time, a company’s valuation multiple will contract and will then trade between 25 to 40 times free cash flow. Second let’s assume the business in question can have a 20% free cash flow margin by then. The table below shows a scenario of a...