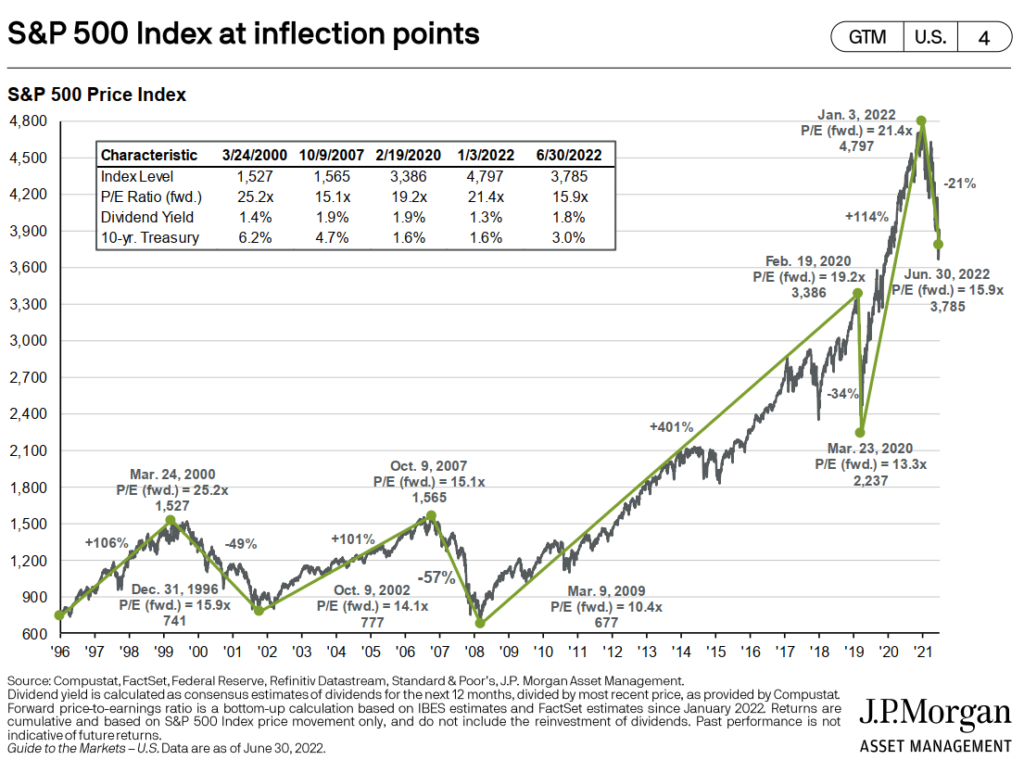

JPMorgan has come up with their third-quarter Guide to the Markets series and out of the slide deck, I think we can take stock of where we are, in terms of market valuation. Since the start of the year, we have seen the forward price-earnings correct from 21.4 times to 15.9 times currently. Interestingly, this is higher than the peak of the Great Financial Crisis in Oct 2007. I think forward price-earnings can only be used as a relative measure of how rich the valuation is and not so much as a tactical allocation tool. Imagine that you are an investor who experienced the 2000 bear and you are in 2007. A forward price-earnings of 15.1 times look reasonable versus the average. Even more so, the forward PE in 2007 is lower than the peak of 2000. Your brain will be told that there is still some way to...

{kind=link}