- Procurri resumed trading following a share placement to meet the regulatory free float requirements.

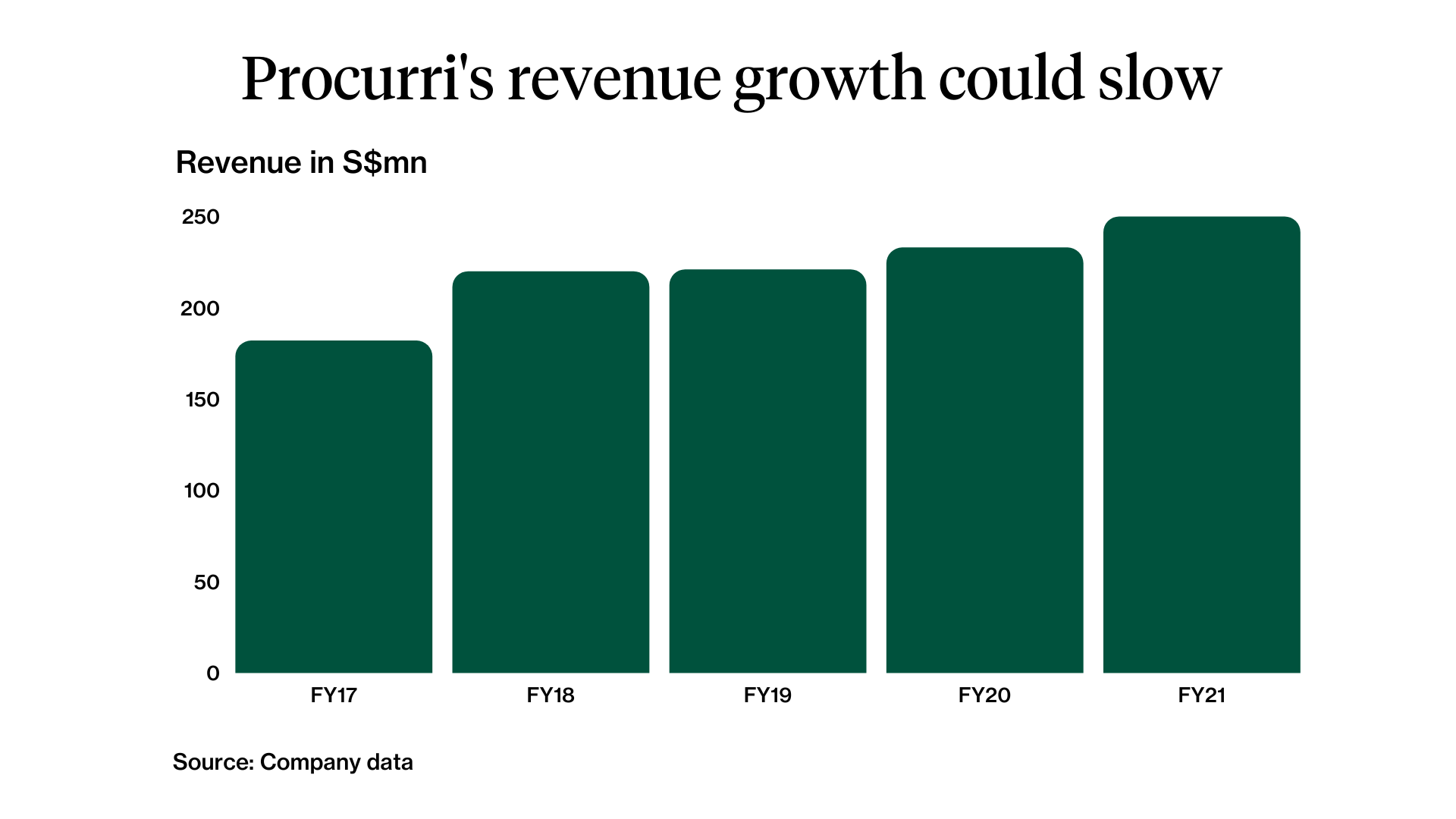

- The company’s revenue growth could slow down with a muted corporate tech spending outlook, as well as a trickling return to offices in the US.

- In addition, its margins could remain weak as tight labour markets in the US and Europe drive up wage costs.

- Procurri is trading at 10x FY21 EV/EBITDA, 37x FY21 PE and 1.4x price to book.

TL;DR