Summary

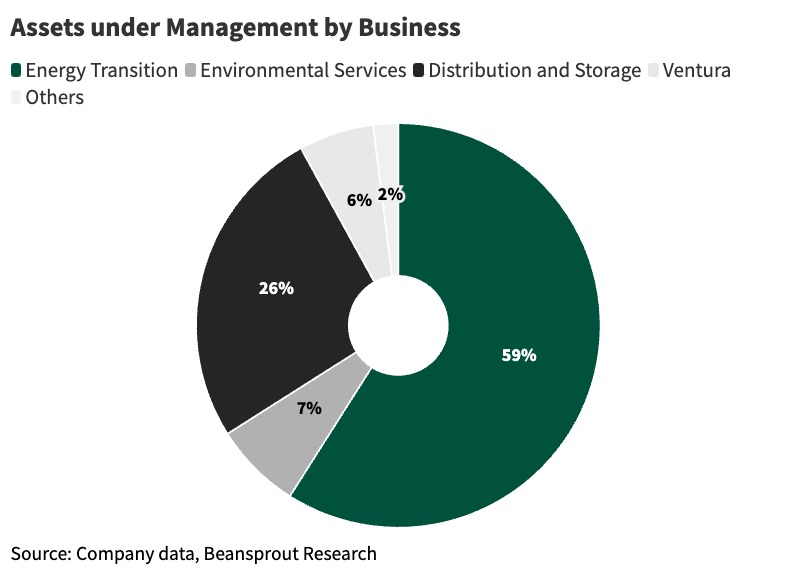

Initiate coverage with BUY. We initiate coverage on Keppel Infrastructure Trust (KIT) with a BUY rating. KIT invests in infrastructure assets in developed markets that provide stable cash flows. About 65% of its revenue is linked to the CPI with cost pass-through. Assets under management reached S$8.7 billion as at end-March 2024.

Distributions expected to grow. Excluding the one-off special dividend paid in FY23, we expect distribution per unit to rise in the next two years. Underpinning this will be: 1) a resumption of distribution from Keppel Merlimau Cogen Plant; 2) contributions from newly-acquired German solar plant; and 3) contributions from Ventura Bus operations in Victoria, Australia from 2H24.

Optimise debt/equity mix to boost returns. As a business trust, KIT is not subject to the regulatory gearing cap. Total debt to total assets was 48.6% as at end-March 2024. This was well below bank covenants. The average cost of debt was

...