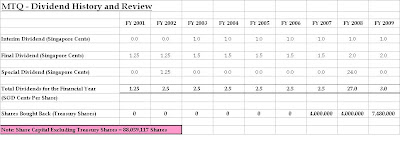

Dividend History

From the available records, it shows that MTQ has been paying dividends consistently since FY 2001, starting from 1.25 cents and increasing this to 2.5 cents per share yearly. Dividends started being paid from FY 2001 onwards (there were no dividends declared for FY 2000). Twice-yearly dividends have been declared since FY 2003 and have been continuing since then.

As for FY 2008, the 24-cent special dividend was declared due to the exceptional gain from the sale of RCR Tomlinson. Subsequently, gross dividend per share was raised to 3 cents per share for FY 2009.

With the onset of the global financial crisis and the expected slowdown in MTQ’s business, FY 2010 may see dividend falling to 2 cents per share. Coupled with their proposed investment in Bahrain of US$20 million, they may decide to conserve more cash. The mode of financing for the Bahrain expansion has yet to be worked out, but will consist of a mixture of internal cash flows and bank borrowings.

One wild card is their investment in Hai Leck (5.02% currently). Seeing Management’s savvy divestment of RCR Tomlinson makes me believe that they may have enough foresight and acumen to know when to divest Hai Leck and to recognize a decent gain, and a special dividend may be declared in future based on this. Read more...

Dividend History

From the available records, it shows that MTQ has been paying dividends consistently since FY 2001, starting from 1.25 cents and increasing this to 2.5 cents per share yearly. Dividends started being paid from FY 2001 onwards (there were no dividends declared for FY 2000). Twice-yearly dividends have been declared since FY 2003 and have been continuing since then.

As for FY 2008, the 24-cent special dividend was declared due to the exceptional gain from the sale of RCR Tomlinson. Subsequently, gross dividend per share was raised to 3 cents per share for FY 2009.

With the onset of the global financial crisis and the expected slowdown in MTQ’s business, FY 2010 may see dividend falling to 2 cents per share. Coupled with their proposed investment in Bahrain of US$20 million, they may decide to conserve more cash. The mode of financing for the Bahrain expansion has yet to be worked out, but will consist of a mixture of internal cash flows and bank borrowings.

One wild card is their investment in Hai Leck (5.02% currently). Seeing Management’s savvy divestment of RCR Tomlinson makes me believe that they may have enough foresight and acumen to know when to divest Hai Leck and to recognize a decent gain, and a special dividend may be declared in future based on this. Read more...This is part 3 of my analysis of purchase for MTQ and it will discuss dividend history, share buy-backs, insider purchases and prospects in Bahrain. A pros and cons analysis will follow to show how this led to my final decision to purchase shares in the company.

Dividend History

From the available records, it shows that MTQ has been paying dividends consistently since FY 2001, starting from 1.25 cents and increasing this to 2.5 cents per share yearly. Dividends started being paid from FY 2001 onwards (there were no dividends declared for FY 2000). Twice-yearly dividends have been declared since FY 2003 and have been continuing since then.

As for FY 2008, the 24-cent special dividend was declared due to the exceptional gain from the sale of RCR Tomlinson. Subsequently, gross dividend per share was raised to 3 cents per share for FY 2009.

With the onset of the global financial crisis and the expected slowdown in MTQ’s business, FY 2010 may see dividend falling to 2 cents per share. Coupled with their proposed investment in Bahrain of US$20 million, they may decide to conserve more cash. The mode of financing for the Bahrain expansion has yet to be worked out, but will consist of a mixture of internal cash flows and bank borrowings.

One wild card is their investment in Hai Leck (5.02% currently). Seeing Management’s savvy divestment of RCR Tomlinson makes me believe that they may have enough foresight and acumen to know when to divest Hai Leck and to recognize a decent gain, and a special dividend may be declared in future based on this. Read more...

Dividend History

From the available records, it shows that MTQ has been paying dividends consistently since FY 2001, starting from 1.25 cents and increasing this to 2.5 cents per share yearly. Dividends started being paid from FY 2001 onwards (there were no dividends declared for FY 2000). Twice-yearly dividends have been declared since FY 2003 and have been continuing since then.

As for FY 2008, the 24-cent special dividend was declared due to the exceptional gain from the sale of RCR Tomlinson. Subsequently, gross dividend per share was raised to 3 cents per share for FY 2009.

With the onset of the global financial crisis and the expected slowdown in MTQ’s business, FY 2010 may see dividend falling to 2 cents per share. Coupled with their proposed investment in Bahrain of US$20 million, they may decide to conserve more cash. The mode of financing for the Bahrain expansion has yet to be worked out, but will consist of a mixture of internal cash flows and bank borrowings.

One wild card is their investment in Hai Leck (5.02% currently). Seeing Management’s savvy divestment of RCR Tomlinson makes me believe that they may have enough foresight and acumen to know when to divest Hai Leck and to recognize a decent gain, and a special dividend may be declared in future based on this. Read more...

Dividend History

From the available records, it shows that MTQ has been paying dividends consistently since FY 2001, starting from 1.25 cents and increasing this to 2.5 cents per share yearly. Dividends started being paid from FY 2001 onwards (there were no dividends declared for FY 2000). Twice-yearly dividends have been declared since FY 2003 and have been continuing since then.

As for FY 2008, the 24-cent special dividend was declared due to the exceptional gain from the sale of RCR Tomlinson. Subsequently, gross dividend per share was raised to 3 cents per share for FY 2009.

With the onset of the global financial crisis and the expected slowdown in MTQ’s business, FY 2010 may see dividend falling to 2 cents per share. Coupled with their proposed investment in Bahrain of US$20 million, they may decide to conserve more cash. The mode of financing for the Bahrain expansion has yet to be worked out, but will consist of a mixture of internal cash flows and bank borrowings.

One wild card is their investment in Hai Leck (5.02% currently). Seeing Management’s savvy divestment of RCR Tomlinson makes me believe that they may have enough foresight and acumen to know when to divest Hai Leck and to recognize a decent gain, and a special dividend may be declared in future based on this. Read more...