In a two-part series, we explore the world of ILPs, or investment-linked plans. In this first part, we talk to asset allocation specialist Brendan Yong and discuss his distaste for ILPs.

—

Could you give one single compelling argument why ILPs are bad for the average person?

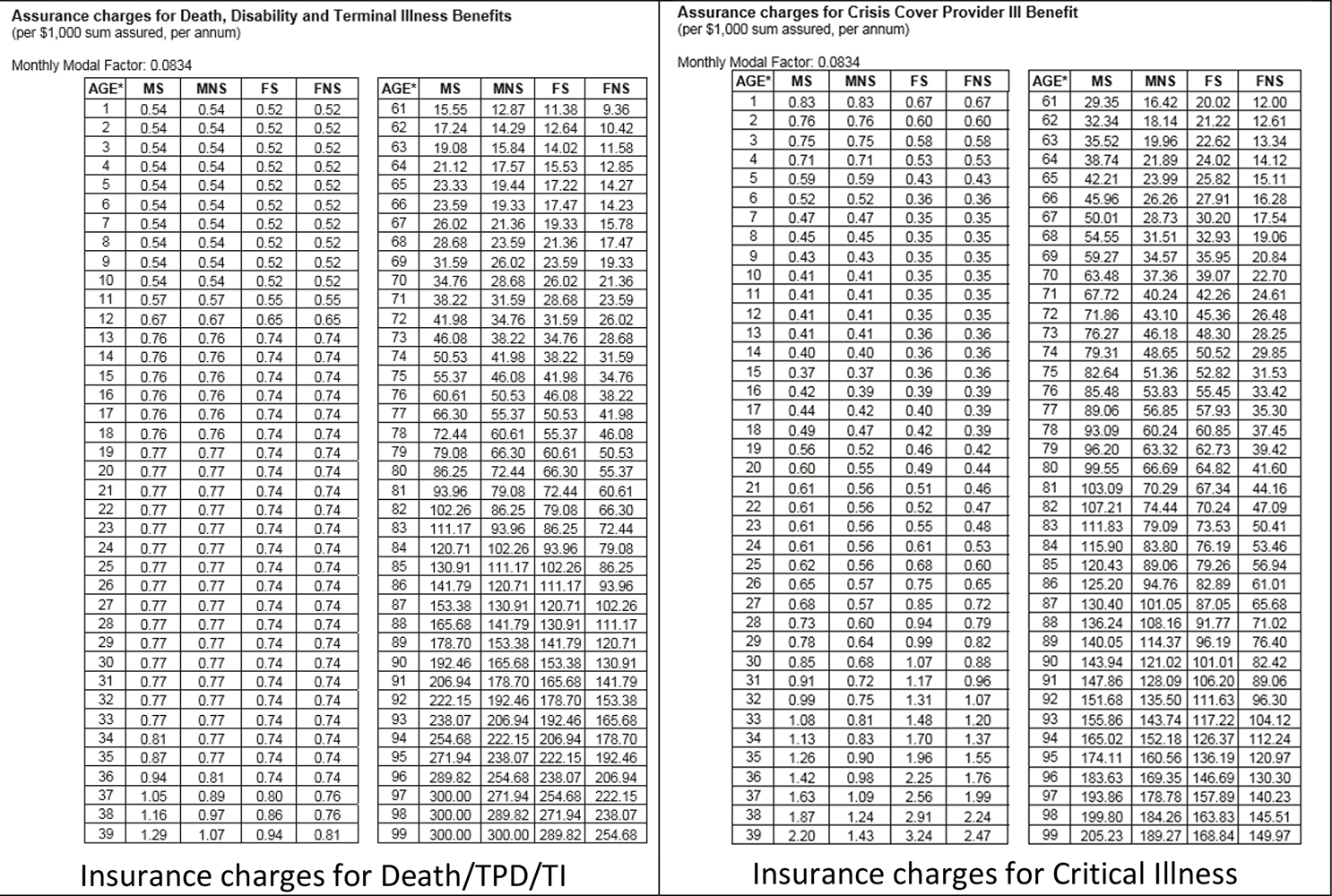

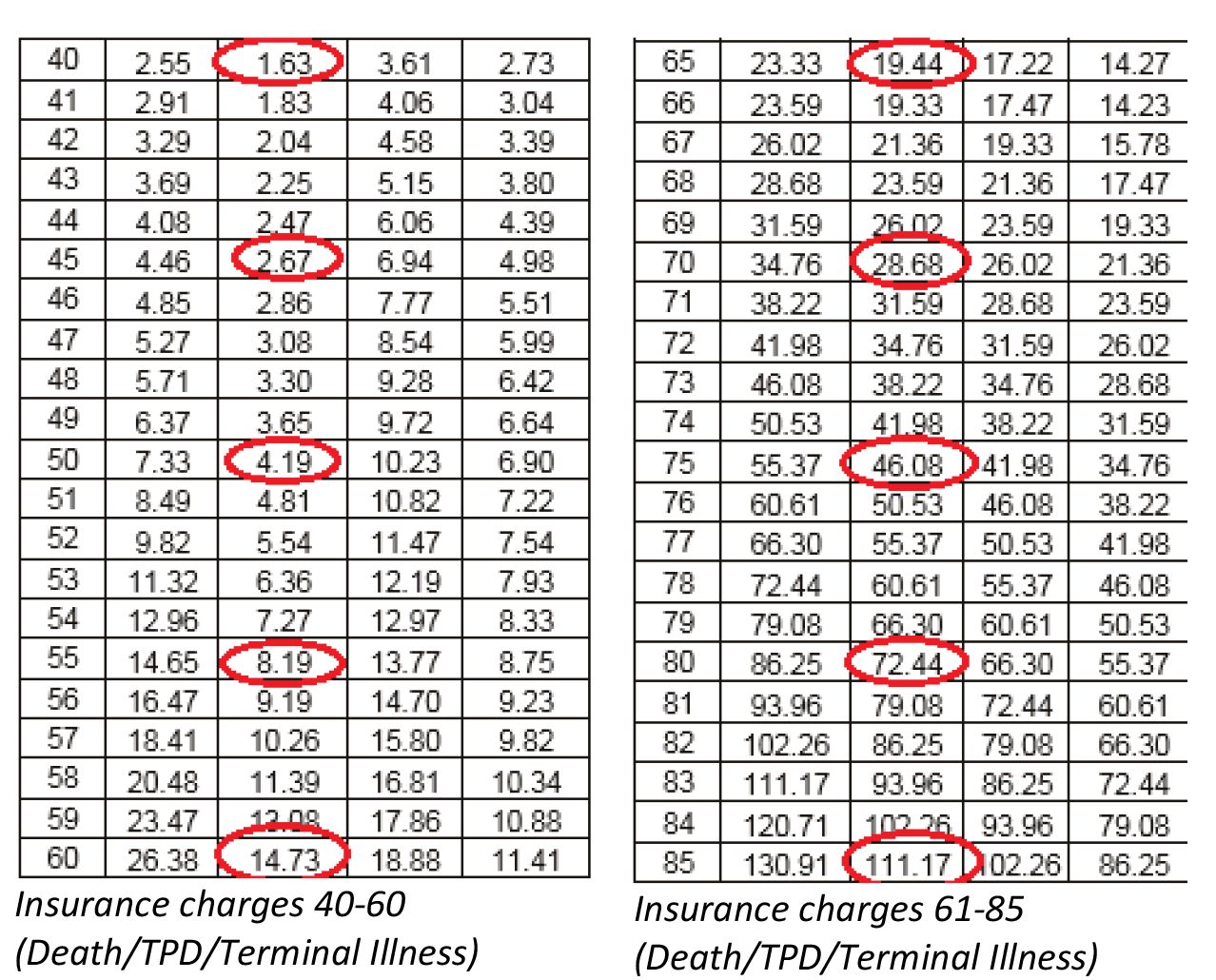

Brendan: It’s just not cost effective. In an ILP, your premium is split between the cost of insurance and the cost of unit trusts. As you age, your insurance cost rises exponentially and the difference becomes quite substantial when you reach the age of 50. Here are a sample of insurance charges from one insurer (click on the image to expand):

The numbers circled in red are the ones that you need to take note of.

For a basic protection plan worth S$100,000 for a male non-smoker, these are the annual costs of insurance with critical illness insurance charges added......

Invest

What is the optimal number of stocks for your portfolio?

By The Fifth Person • April 26, 2024

Invest

What is the optimal number of stocks for your portfolio?

By The Fifth Person • April 26, 2024