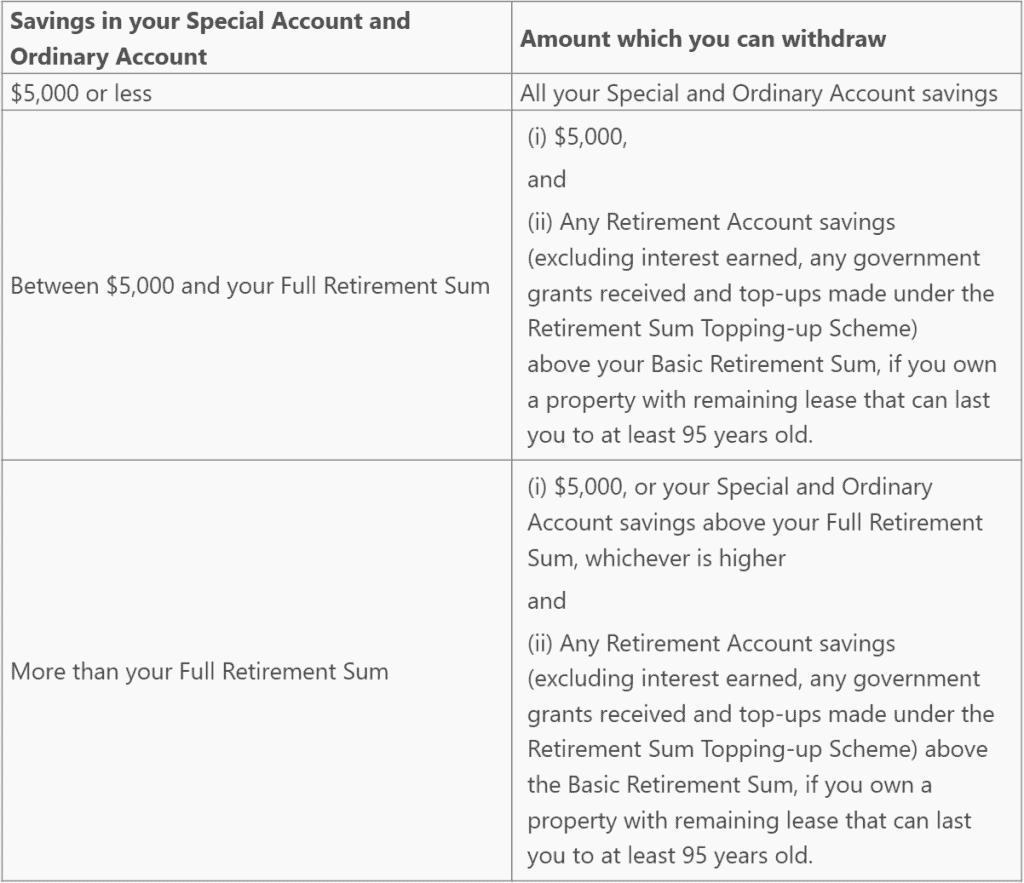

- How much can you withdraw from your SA/OA after setting aside FRS in your RA?

- How much can you withdraw from your RA if you pledge your property, thus setting aside BRS amount instead?

- Could you withdraw ALL the difference between FRS and BRS? Or some? Otherwise how come none in other scenarios?

- How is mandatory contribution (employer/employee) treated differently from OA to SA transfers and RSTU cash top-up? Or how similar are they treated in the calculation of RA withdrawal?

I wanted to strengthen my understanding as well as my readers’ on CPF lump sum withdrawal from age 55 after my last post on whether you can withdraw ALL excess money from your CPF SA / OA account after meeting FRS / BRS. Some questions got me thinking, but I thought that just thinking ain’t going to get me far in my understanding without playing out the various scenarios applicable with real numbers.