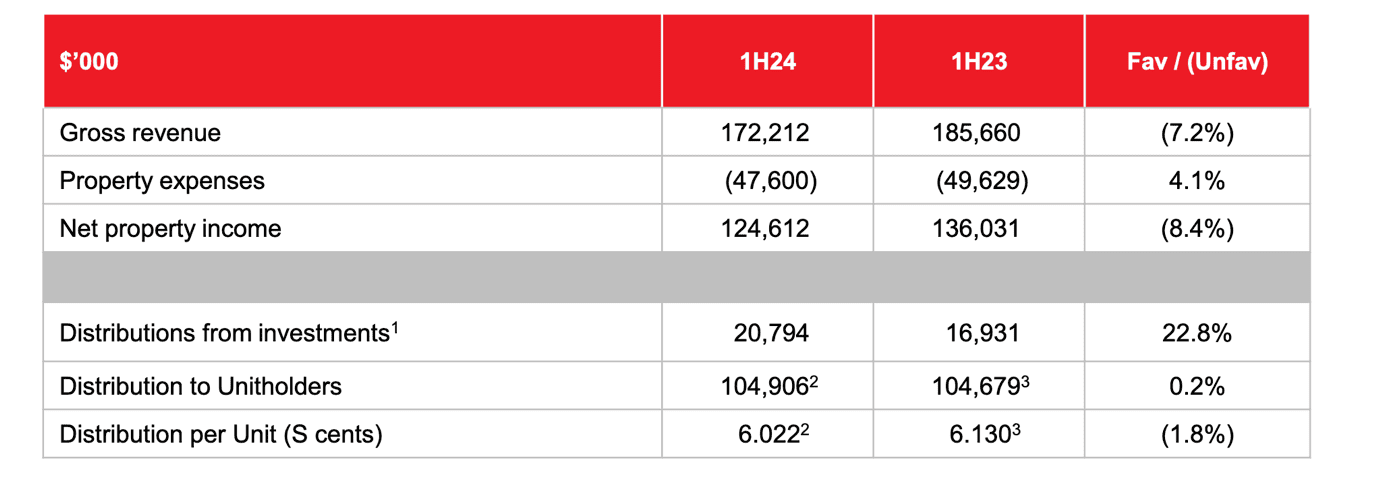

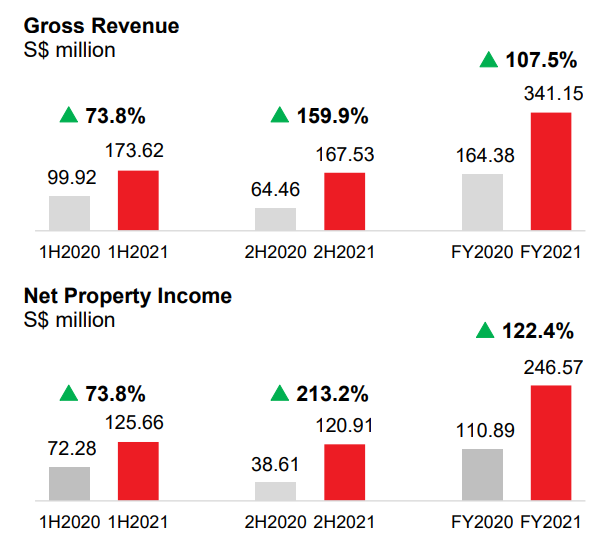

Frasers Centrepoint Trust announced a good set of numbers for FY2021, where Revenue and Net Property Income ("NPI") more than doubled following the ARF acquisitions.

The 2H performance was weaker due to rental rebates and additional tenant assistance provided. Having said that, the Distribution Per Unit ("DPU") for the current year, improved by 33.7% to 12.085 Singapore cents. You can find the management presentation here.

Based on the DPU of 12.085 cents and the closing price of $2.27 on 30 Sep 2021, the trading yield was around 5.3%.

The distribution for 1 April to 30 Sep is 6.089 Singapore cents and the book will close on 5 Nov and be paid out on 29 Nov 2021.

Based on my 30,000 units in my SRS portfolio, the distribution will be $1,826.70.

For those not familiar with FCT, it is basically a pure play Singapore suburban retail REIT.

The gearing ratio remained conservative at 33.3% and the occupancy remained resilient at 97.3%. The NAV per unit is around $2.30 as of 30 Sep 2021....