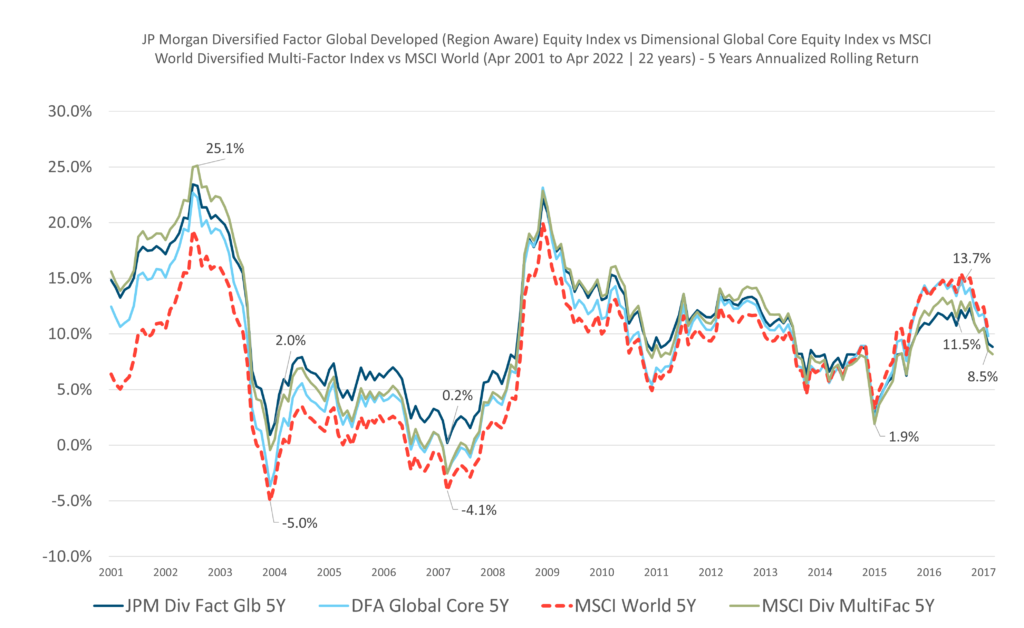

In some of the articles on Smart Beta in the past, I shared that with the additional risk that you take by investing in the value, momentum, quality or size factors, you may be rewarded in the long run by higher returns above the market risk premiums.

If you invest in a Smart Beta fund that screens and invests in stocks that exhibit multiple factors, you may be able to systematically capture the premiums with much smoother returns that do not underperform the index too much.

You might also do better when the main index, such as the MSCI World did not do that well. You can read Would Smart Beta ETF Improve Your Returns If the Market Indices are Not Performing Well?

Over the weekend, I chanced upon the index data behind the JPMorgan ETFs (Ireland) ICAV – Global Equity Multi-Factor UCITS ETF (Ticker: JPGL on Interactive Brokers) and decide to see...