Recently, in forums, there has been a mockery over Singapore entities (such as Temasek) overpaying for their purchases and then delivering low to negative returns (purchase of FTX, TSMC etc). Unfortunately, it seems another Singapore company, this time SATS, is likely to be overpaying for its purchase

$1.82 billion purchase of WFS

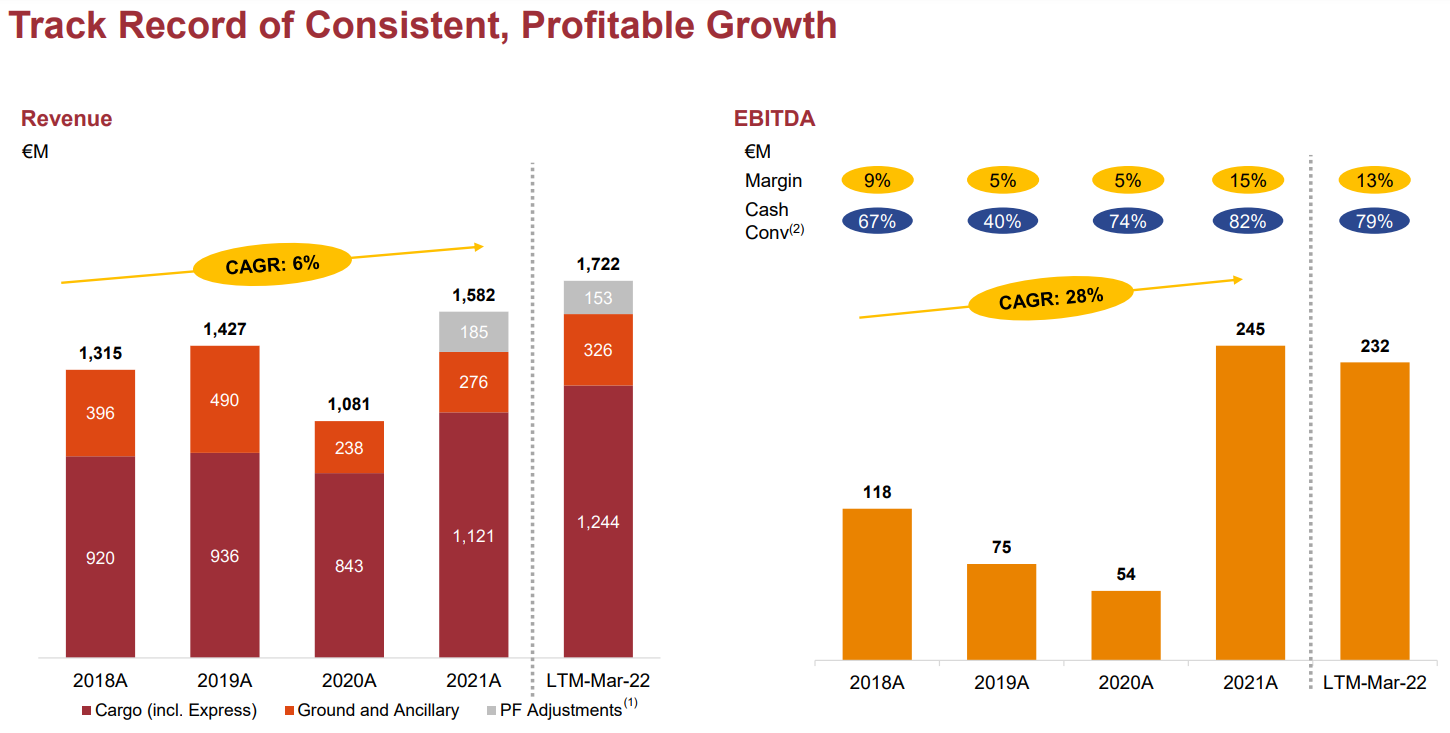

WFS is a air cargo company. Due to the e commerce boom arising from the need to stay at home during COVID,many air cargo firms experienced an increase in profit margins as the boom in e commerce was constrained by airline slots. Even Singapore Airlines (SIA) experienced a boom in air cargo business. However, in recent quarters, SIA is now reporting a decreasing air cargo volume. Given that SATS and SIA are closely linked, I am surprised that SATS still went on for the pruchase of WFS.

From WFS's financial reports, EBITDA profits is falling and this is due...