Its absolutely surprising to see a SGX listed REIT valued at almost a 24% dividend yield. It will take only about 4-5 years to recuperate your capital and to add to that, the REIT's properties are freehold in nature! That means a perpetual 20+% dividend yielder.

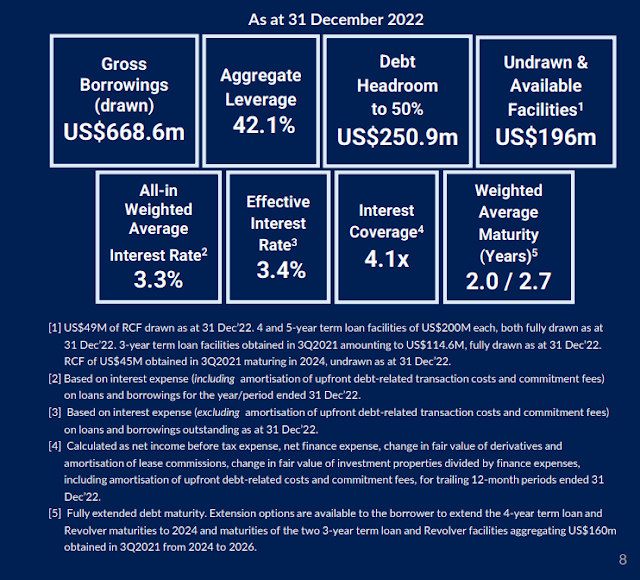

Let's see a screenshot of the current financial situation of PRIME US REIT:

It seems the market feels the REIT manager of PRIME is not seemingly doing a good job and the US commercial market it is in terrible shape. Let's look at a few factors which could explain the current pricing.

Poor US Commercial Real Estate Market and Overleveraged

A simple google search will show that the US office space is hit with double digits vacancy and falling valuations. PRIME and Manulife REIT are reporting downward valuation of their properties; the chief reason is due to the higher risk free rates that their valuers used. Keppel Pac Oak on the other hand...