Buy-to-let property is a wealth machine that many in Singapore or Asia think is ideal for their retirement income. (In case you are new to the concept of wealth machines, you can

read it here)

I am okay with that as a wealth machine.

It is just that how do you plan your financial independence, or retirement with the income from a buy-to-let property?

There are two questions we need to contend with:

- What is the starting income that you use to plan?

- How does the income grow from the start and over time?

Answering these two questions have critical outcome to whether your plan work or not.

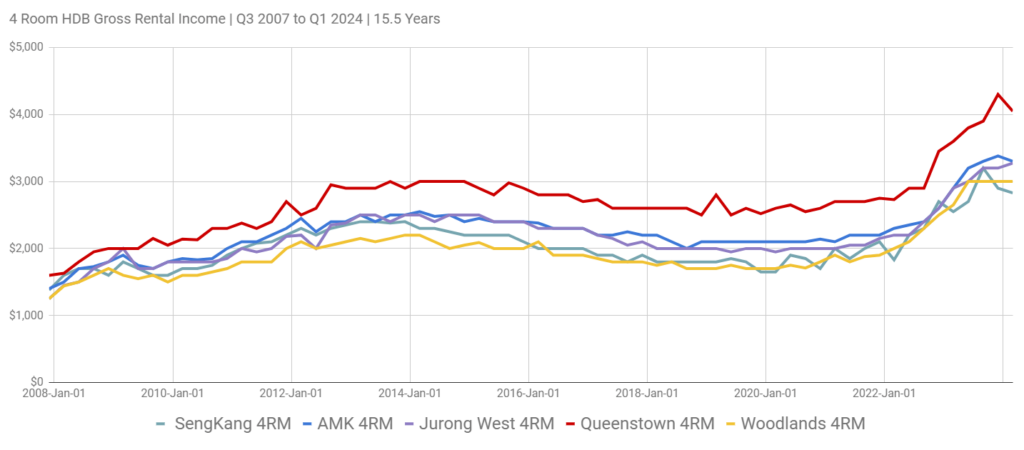

The very common assumptions used in planning:

- The current rental yield that the client or prospect has secured.

- An assume annual growth rate of 2-3% p.a.

Are these planning assumptions sound? I don’t know.

If we look at the data, planning like this may result in a mismatch in your expectations compare to the reality....