Please read the disclaimer at the bottom of my blog if you wish to continue with the contents below.

The market is valuing ST Engineering at 5.31x books. EPS CAGR for 3 years is at +4.93%. If it is able to maintained its DPS at 15cts, its yield will be around 4.48%. Lets take a look at its financials:Sembcorp and Sembmarine were excluded from the table because their latest quarter were net debt positive. What I did here was to collate all the blue chips with zero net debt and align them in an ascending rolling PE order(as shown above). The top three are the bank counters(OCBC, DBS, UOB) which have moved up recently. The counter with PE<20x and price closest to its 52 Wks Low is ST Engineering. Is it trading at a hefty discount now?

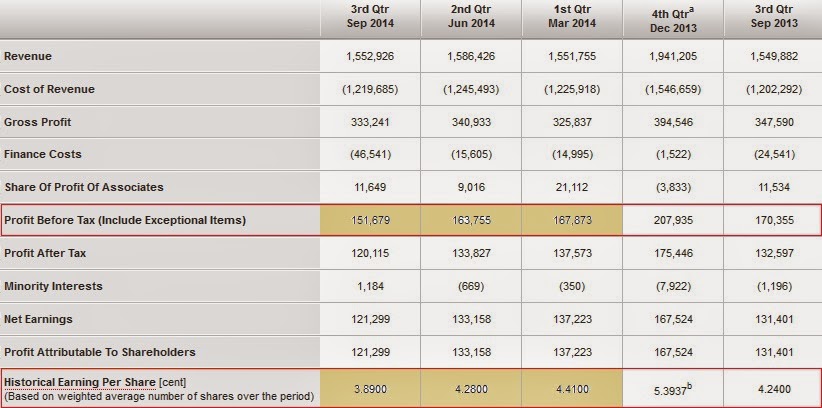

|

| Collated using Shareinvestor |

The above table shows ......