Ascendas REIT has recently replaced CapitaLand Mall Trust as Singapore's largest capitalised REIT – and has been the second-best performing REIT in the YTD with an 11.9% total return.

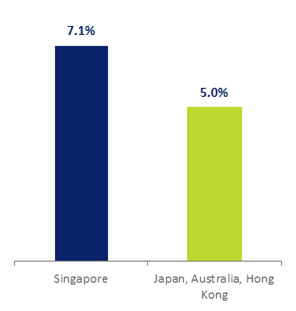

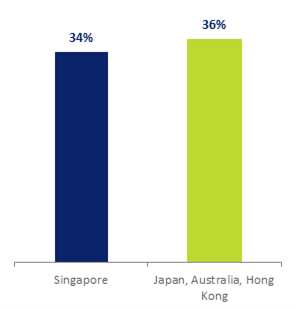

The capitalisation of Singapore’s REIT Sector has almost doubled over the past five years. Singapore’s REIT Sector also maintains a competitive edge with higher average yields and lower average gearing ratios than the combined REIT Sector of Japan, Australia and Hong Kong.

The NikkoAM - StraitsTrading Asia ex Japan REIT ETF which is expected to include up to 70% weightage in Singapore REITs is scheduled to list on SGX on 29 March 2017. Ascendas REIT and CapitaLand Mall Trust are expected to maintain relatively large weightings in the ETF.

Ascendas REIT has recently become Singapore’s largest REIT by market capitalisation, with a capitalisation of S$7.2 billion. CapitaLand Mall Trust with a capitalisation of S$6.9 billion remained Singapore’s largest REIT by total assets at the end of 2016, in addition to the largest retail REIT by market capitalisation.

As of 31 December 2016, CapitaLand Mall Trust maintained total assets of $10.3 billion while Ascendas REIT maintained total assets of S$9.7 billion. Last month, Ascendas REIT completed the acquisition of 12, 14 and 16 Science Park Drive and issuance of consideration units.

Ascendas REIT and CapitaLand Mall Trust – Management Outlook

Both REITs are leaders in their fields of Retail-related property and Industrial property. As noted by the

Ministry of Trade and Industry, the Singapore economy has slowed down and is expected to grow at 1.0% to 3.0% in 2017.

Ascendas REIT noted in their recent financial reports:

- JTC estimated island-wide vacancy for industrial property has risen to 10.9% as at December 2016- furthermore, new supply of about 2.2 million square metres of industrial space in 2017 will put further pressure on occupancy and rental rates.

- Ongoing stringent subletting policy, shrinking space requirement by existing and new tenants, and a trend by the government is to sell shorter lease industrial land.

- To enhance the stability and sustainability of returns, Ascendas REIT plans to continue to invest in properties with long remaining land lease tenures (its portfolio weighted average land lease to expiry is about 46 years).

- For its Australia portfolio, Ascendas REIT noted consensus 2017 GDP growth is forecast to be stable at approximately 2.6%, as the Australian economy continues to make a transition from resources to a broader range of industries.

Ascendas REIT also acknowledged that higher interest rates will result in higher interest expense and lower distributions per unit (DPU). To mitigate interest rates volatility, about 82.7% of Ascendas REIT’s borrowings have been hedged and new acquisitions feasibility will have to factor in the potential higher interest rates and impact.

The Manager of CapitaLand Mall Trust also acknowledged softer economic conditions and noted that going forward it will continue to focus on sustaining DPU. CapitaLand Mall Trust’s portfolio of quality shopping malls are well-connected to public transportation hubs and are strategically located either in areas with large population catchments or within Singapore’s popular shopping and tourist destinations.

For FY 2016, its tenants’ sales per square foot and shopper traffic increased 0.9% and 2.3% respectively year-on-year. Coupled with the large and diversified tenant base of the portfolio, the Manager of CapitaLand Mall Trust noted that the strategic locations will contribute to the stability and sustainability of the malls’ occupancy rates and rental revenues.

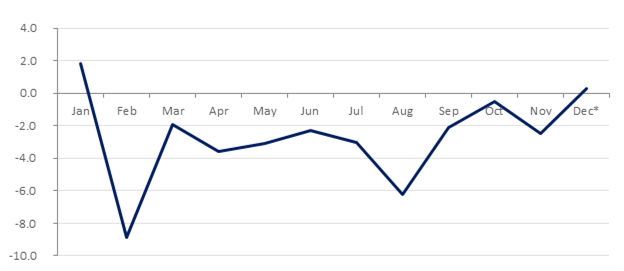

The increase in Tenants’ sales per square foot and shopper traffic increased despite year-on-year (YoY) declines of Singapore’s Retail Sales Index (excluding motor vehicles) as illustrated below.

Monthly Percentage Change in Retail Sales Index (excl. Motor Vehicles) YoY

Source: Department of Statistics Singapore (click

here), Note* preliminary

In December, the Retail Sales Index (excl. Motor Vehicles) generated a preliminary expansion of 0.3% YoY.

As illustrated above, YoY declines of the in Retail Sales Index (excl. Motor Vehicles) were progressively less over 2016. The data for this Index is collected through monthly surveys of retail establishments that sell merchandise directly to consumers. Total retail sales in Singapore for the month of December was estimated to be S$4.2 billion in December 2016, similar to December 2015.

SGX REIT Sector Maintains Competitive Edge

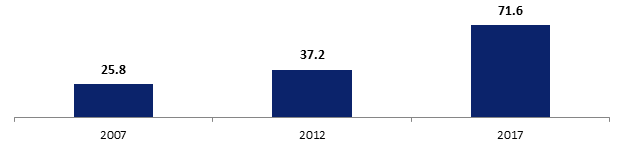

Singapore lists 32 Real Estate Investment Trusts (REITs) and six stapled trusts with a combined market capitalisation of S$71.6 billion. All 38 of these trusts have generated positive returns in the 2017 year through to the 6 March close, with the average total return at 5.4%. This average gain in-line with the average total returns of REITs listed in Japan, Australia and Hong Kong.

The combined market capitalisation of Singapore’s REIT Sector has almost doubled over the past five years. Together, the 32 REITS and six stapled trusts now represent 8% of Singapore’s total market capitalisation. REITs began listing in Singapore in 2002 with the listing of CapitaLand Mall Trust and Ascendas REIT. While the Sector has expanded significantly over the past five years, the competitive edge of high distribution yields and lower gearing ratios has been maintained.

Market Capitalisation of the SGX REIT Sector (S$ Billion)

Source: SGX, Bloomberg (Data as of 6 March 2017)

| REIT Sector Average Dividend Yields |

REIT Sector Average Total Debt to Total Assets |

|

|

Source: SGX, Bloomberg (Data as of March 2017), Data based on GICS ® Sectors.

NikkoAM - StraitsTrading Asia ex Japan REIT ETF

The NikkoAM - StraitsTrading Asia ex Japan REIT ETF was put up for initial offer on 6 March and is targeted to list on SGX on 29 March, 2017.

This new Exchange Traded Fund (ETF) tracks the performance of the FTSE EPRA/NAREIT Asia ex Japan Net Total Return REIT Index, which has estimated 70% exposure to Singapore listed REITs. The Index also and has an indicative net dividend yield of more than 5% per annum (click

here to read more).

The ETF gives easy access to diverse properties such as financial hubs, tech hubs, hospitals, residential and industrial properties, malls and hotels, diversified geographically across Asia ex Japan within a single trade and will also be an EIP ETF.

The ETF is open for subscription via DBS Vickers, OCBC Securities, Phillip Securities and UOB Kay Hian until 21 March 2017. This will be the third ETF by Nikko AM listed on SGX next to the ABF Singapore Bond Fund and NikkoAM STI ETF. The NikkoAM - StraitsTrading Asia ex Japan REIT will also be the second SGX listed ETF to be focused on REITs.

Recent Performance of Singapore REITs

As noted above all 38 of the trusts have generated positive returns in the 2017 year through to the 6 March close. The five best performing of the 38 trusts in the year thus far were Sabana Shari'ah Compliant Industrial REIT, Ascendas REIT, Lippo Malls Indonesia Retail Trust, Cambridge Industrial Trust and CDL Hospitality Trusts.

The tables below details the 38 trusts below and is sort by market capitalisation. Click on each stock to visit its profile page on SGX Stock Facts.

| Name |

SGX Code |

Price last close S$ |

Market Cap S$M |

Total Return YTD % |

Total Return 1 Yr % |

P/B |

P/B 5Yr Avg |

Dvd Ind Yld % |

| Ascendas REIT |

A17U |

2.480 |

7,177 |

11.9 |

9.4 |

1.2 |

1.2 |

6.2 |

| CapitaLand Mall Trust |

C38U |

1.935 |

6,895 |

4.2 |

-5.9 |

1.0 |

1.1 |

6.0 |

| CapitaLand Commercial Trust |

C61U |

1.530 |

4,584 |

6.6 |

10.0 |

0.9 |

0.8 |

6.1 |

| Suntec REIT |

T82U |

1.740 |

4,453 |

7.0 |

7.9 |

0.8 |

0.8 |

6.0 |

| Mapletree Commercial Trust |

N2IU |

1.480 |

4,278 |

7.7 |

9.9 |

1.1 |

1.1 |

5.6 |

| Keppel REIT |

K71U |

1.020 |

3,385 |

1.5 |

11.1 |

0.7 |

0.7 |

5.8 |

| Mapletree Industrial Trust |

ME8U |

1.685 |

3,010 |

4.2 |

15.4 |

1.2 |

1.2 |

6.7 |

| Fortune REIT |

F25U |

1.576 |

2,981 |

0.8 |

15.3 |

0.7 |

0.6 |

5.6 |

| Mapletree GCC Trust |

RW0U |

0.985 |

2,753 |

3.7 |

12.8 |

0.8 |

0.8 |

7.3 |

| Mapletree Logistics Trust |

M44U |

1.060 |

2,663 |

5.8 |

16.1 |

1.0 |

1.0 |

7.1 |

| SPH REIT |

SK6U |

0.970 |

2,464 |

3.5 |

6.9 |

1.0 |

1.0 |

5.6 |

| Ascott Residence Trust |

A68U |

1.170 |

1,952 |

7.5 |

10.9 |

0.9 |

0.8 |

7.6 |

| Frasers Centrepoint Trust |

J69U |

2.010 |

1,849 |

7.3 |

8.8 |

1.0 |

1.1 |

5.8 |

| Starhill Global REIT |

P40U |

0.745 |

1,625 |

2.4 |

4.6 |

0.8 |

0.8 |

6.8 |

| Parkway Life REIT |

C2PU |

2.440 |

1,476 |

4.7 |

6.8 |

1.4 |

1.4 |

5.0 |

| CDL Hospitality Trusts* |

J85 |

1.390 |

1,395 |

7.9 |

14.3 |

0.9 |

0.9 |

8.0 |

| Frasers Logistics & Industrial |

BUOU |

0.960 |

1,336 |

3.8 |

N/A |

1.0 |

N/A |

N/A |

| Keppel DC REIT |

AJBU |

1.165 |

1,313 |

0.6 |

17.6 |

1.2 |

1.2 |

5.3 |

| OUE Hospitality Trust* |

SK7 |

0.695 |

1,251 |

7.4 |

3.8 |

0.9 |

0.8 |

7.9 |

| Frasers Hospitality Trust* |

ACV |

0.680 |

1,249 |

4.6 |

-1.8 |

0.9 |

0.9 |

9.0 |

| CapitaLand Retail China Trust |

AU8U |

1.420 |

1,241 |

7.2 |

4.2 |

0.9 |

0.9 |

6.7 |

| Lippo Malls Indonesia Retail Trust |

D5IU |

0.395 |

1,108 |

9.1 |

35.4 |

1.0 |

0.9 |

8.9 |

| Far East Hospitality Trust* |

Q5T |

0.590 |

1,056 |

0.2 |

-1.7 |

0.6 |

0.7 |

7.6 |

| Frasers Commercial Trust |

ND8U |

1.265 |

1,014 |

2.4 |

6.9 |

0.8 |

0.8 |

7.9 |

| First REIT |

AW9U |

1.280 |

992 |

2.9 |

15.2 |

1.3 |

1.2 |

6.7 |

| OUE Commercial REIT |

TS0U |

0.695 |

912 |

3.6 |

11.0 |

0.8 |

0.7 |

7.2 |

| AIMS AMP Capital Industrial REIT |

O5RU |

1.350 |

862 |

5.2 |

7.2 |

0.9 |

0.9 |

8.2 |

| Ascendas Hospitality Trust* |

Q1P |

0.755 |

849 |

7.1 |

5.9 |

0.9 |

0.9 |

7.1 |

| Viva Industrial Trust* |

T8B |

0.780 |

752 |

4.7 |

20.5 |

1.0 |

0.9 |

8.9 |

| Cambridge Industrial Trust |

J91U |

0.575 |

750 |

8.4 |

13.8 |

0.9 |

0.8 |

7.0 |

| Manulife US REIT |

BTOU |

1.187 |

739 |

3.6 |

N/A |

1.1 |

N/A |

N/A |

| Cache Logistics Trust |

K2LU |

0.815 |

738 |

2.9 |

3.7 |

1.1 |

1.0 |

9.1 |

| Soilbuild Business Space REIT |

SV3U |

0.645 |

674 |

3.3 |

-1.4 |

0.9 |

0.9 |

9.7 |

| EC World REIT |

BWCU |

0.765 |

576 |

2.6 |

N/A |

N/A |

N/A |

N/A |

| IREIT Global |

UD1U |

0.725 |

473 |

5.8 |

15.2 |

1.2 |

1.1 |

8.6 |

| Sabana Shari'ah Compliant Industrial REIT |

M1GU |

0.475 |

453 |

27.9 |

-7.1 |

0.6 |

0.7 |

7.5 |

| BHG Retail REIT |

BMGU |

0.670 |

332 |

2.3 |

-12.9 |

0.8 |

N/A |

8.1 |

| Saizen REIT |

T8JU |

0.053 |

15 |

3.9 |

42.9 |

1.7 |

1.2 |

N/A |

| Average |

|

|

|

5.4 |

9.5 |

1.0 |

0.9 |

7.1 |

Source: SGX, Bloomberg & SGX StockFacts (data as of 6 March 2017), Note dividend yields for trusts listed for less than 12 months are not included* Stapled Trusts. Note table does not include five Business Trusts investing in property-related Assets – Ascendas India Trust, Indiabulls Properties Investment Trust, Religare Health Trust, Croesus Retail Trust and Dasin Retail Trust.

Risks

The risks associated with a REIT investment vary and depend on the unique characteristics each REIT (such as its. leverage ratio, cost of refinancing, alignment of management fees), as well as the geographical location and quality of the underlying property investments such as concentration of properties and the length of leases.

Other risks associated with stock investing such as price risk, volatility and liquidity risks also apply. Investors should study the specific REIT prospectus to understand its investment objective and details of the properties to be acquired before making an investment decision.

SGX My Gateway

SGX’s investor education portal with market, product and investment information and events. Sign up now at

sgx.com/mygateway to receive our investment updates and economic calendar.

This document is not intended for distribution to, or for use by or to be acted on by any person or entity located in any jurisdiction where such distribution, use or action would be contrary to applicable laws or regulations or would subject SGX to any registration or licensing requirement. This document is not an offer or solicitation to buy or sell, nor financial advice or recommendation for any investment product. This document has been published for general circulation only. It does not address the specific investment objectives, financial situation or particular needs of any person. Advice should be sought from a financial adviser regarding the suitability of any investment product before investing or adopting any investment strategies. Investment products are subject to significant investment risks, including the possible loss of the principal amount invested. Past performance of investment products is not indicative of their future performance. While SGX and its affiliates have taken reasonable care to ensure the accuracy and completeness of the information provided, they will not be liable for any loss or damage of any kind (whether direct, indirect or consequential losses or other economic loss of any kind) suffered due to any omission, error, inaccuracy, incompleteness, or otherwise, any reliance on such information. Neither SGX nor any of its affiliates shall be liable for the content of information provided by third parties. SGX and its affiliates may deal in investment products in the usual course of their business, and may be on the opposite side of any trades. SGX is an exempt financial adviser under the Financial Advisers Act (Cap. 110) of Singapore. The information in this document is subject to change without notice.