When M1 announced its results in end Jan, I went to buy both M1 and Singtel, but I did not buy Starhub. The conventional wisdom is that between M1 and Starhub, Starhub would be better able to manage the competition from the fourth telco, as it has Pay TV, broadband and enterprise fixed services besides mobile services. That is true provided the other business segments are generating stable, recurrent cashflows. However, is that true?

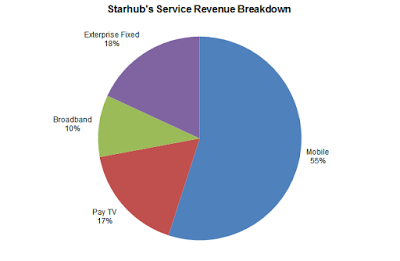

First of all, let us look at the revenue contribution from its 4 business segments.

| |

| Fig. 1: Starhub's Service Revenue Breakdown |

Excluding equipment sales, mobile services constitute the bulk of Starhub's service revenue in FY2016, contributing 55% of the revenue. The second largest segment is enterprise fixed services, contributing 18%. Pay TV is third with 17% contribution while broadband services is smallest with 10% contribution. Let us look at the prospects of each business segment......