- Global rubber glove industry to post 8%-10% annual growth in the next few years, mainly driven by increasing emerging market demand. Malaysia continues to be the top rubber glove manufacturer globally with c.63.0% market share.

- While near-term headwinds (competition, raw material prices, and currencies) remain, glove manufacturers are positive on structural growth trends of the industry and remain committed to their respective capacity expansion plans.

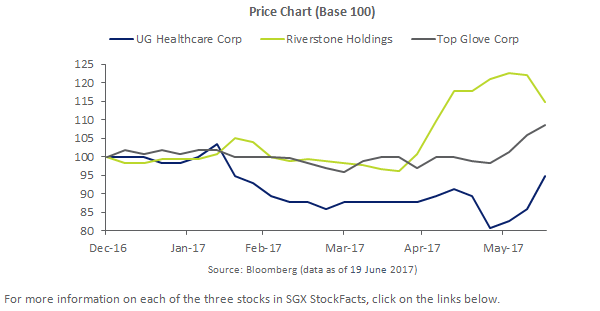

- SGX lists three rubber glove plays with a combined market capitalisation of S$3 billion. Top Glove Corporation is the largest stock in this segment at S$2 billion. The company will host a webinar on 22 June (Thu) to discuss its latest financial results.

The Healthcare Sector in Asia is benefiting from structural growth trends in the industry such as rapidly ageing populations, rising disposable incomes and increasing per capita healthcare spending (click

here for more). The global rubber glove industry is a direct beneficiary of an expanding Healthcare Sector, as rubber gloves are often seen as an indispensable item for hygiene purposes.

Robust Outlook for Global Rubber Glove Industry

According to the Malaysia Rubber Glove Manufacturers Association (MARGMA), the estimated global demand for rubber gloves was at 212.2 billion pieces in 2016. MARGMA added that Malaysia continues to be the number one rubber glove producer globally, with a market share of c.63.0% in 2016. In the longer term, MARGMA expects the global rubber glove industry to maintain strong annual growth of 8%-10% over the coming years, primarily driven by increasing consumption in emerging markets.

Favourable Demand/Supply Dynamics and Easing Price Pressures

According to DBS Vickers Securities, leading glove manufacturers are aiming to raise capacity at a gradual pace to better track demand growth. This will likely help to avoid oversupply conditions and price competition. As demand/supply dynamics turn favourable, glove manufacturers are able to raise average selling prices (ASPs) to offset higher raw material costs. DBS Vickers expects the above two factors to help stabilise glove manufacturers’ margins. This is further helped by continuous efforts in increasing efficiency and automation.

SGX’s Rubber Glove Plays Positive Despite Near-Term Headwinds

Singapore lists three rubber glove manufacturers with a combined market capitalisation of S$3 billion. Top Glove’s results announcement on 16 June 2017 rounded off the reporting season for SGX’s glove manufacturers. While the three companies flagged increasing raw material prices, fluctuating currencies and competition as near-term headwinds, the respective management remain bullish on longer-term growth prospects for the industry and have all committed to plans to expand their production capacity to meet future demand.

| Name |

SGX Code |

Price S$ |

Market Cap S$M |

Total Return YTD % |

Total Return 1 Yr % |

P/E (x) |

Forward P/E (x) |

2017 ROE % |

P/B |

Dvd Ind Yld % |

| Top Glove Corp |

BVA |

1.750 |

2,244 |

7.8 |

N/A |

23.5 |

20.1 |

17.4 |

3.7 |

2.7 |

| Riverstone Hldgs |

AP4 |

1.015 |

748 |

17.6 |

16.8 |

17.9 |

17.4 |

22.5 |

3.9 |

2.1 |

| UG Healthcare Corp |

41A |

0.270 |

52 |

-5.3 |

-11.1 |

14.2 |

16.9 |

N/A |

1.4 |

2.2 |

| Average |

|

|

|

6.7 |

2.9 |

18.5 |

18.1 |

20.0 |

3.0 |

2.3 |

Source: SGX, Bloomberg & SGX StockFacts (data as of 19 June 2017)

Top Glove Corporation

World’s largest rubber glove manufacturer with an annual production capacity of 48 billion pieces per annum from 30 factories.

Recent Earnings Release

- Recently reported 3QFY17 revenue was at RM869.6 million, increasing 2.1% QoQ and 29.3% YoY. Sales volume (quantity sold) declined 5% QoQ and 1% YoY, following an increase in ASP which resulted in the surge in raw material prices, causing orders to be deferred.

- 3QFY17 profit after tax (PAT) of RM77.5 million increased 23.5% YoY despite the spike in both natural rubber latex and nitrile latex prices. PAT in the quarter declined 6.8% QoQ due to time lag in passing on increase in raw material prices to customers and lower volume sold.

- During the quarter, the average natural rubber latex price climbed to RM7.06/kg (+18.6% QoQ, +79.2% YoY). The average nitrile latex price was at US$1.34/kg (+24.1% QoQ, +41.1% YoY). As of 16 June 2017, the natural rubber latex price has decreased to RM5.56/kg. Click here for more details on the results.

Management Outlook and Highlights

- Despite the unfavourable conditions in the industry, the company performed well due to ongoing improvements in its manufacturing process, enabling an efficient management of its costs. Through its good relationship with customers, the company also managed to share the cost increases.

- Management intends to construct three new manufacturing. Upon completion, the factories will boost total number of production lines by an additional 106 lines and production capacity by 10.6 billion gloves annually. The company also acquired two glove factories (combined production capacity of 1.1 billion annually) in May 2017 with a targeted completion in August 2017. By December 2018, management expects Top Glove to have 31 glove factories, 628 production lines and a production capacity of 59.7 billion gloves per annum.

- As of 31 May 2017, Top Glove maintained a positive net cash position of RM95.3 million and declared an interim dividend of RM0.06, payable on 17 July 2017.

- Management expects business environment to remain challenging on volatile currency trends. On a positive note, management noted that raw material prices have been declining since May 2017 and expects stronger volume growth in the coming quarter.

Top Glove Corporation will be hosting a webinar on 22 June (Thu) at 7:30pm (SG time) to discuss its track record, key growth drivers and the latest 3QFY17 financial results. Click

here to register.

To read the SGX

kopi-C profile of Top Glove Corporation Executive Chairman Tan Sri Dr Lim Wee Chai, click

here.

Riverstone Holdings

Leading natural rubber and nitrile (synthetic rubber) glove manufacturer which specialises in cleanroom and healthcare gloves.

Recent Earnings Release

- 1QFY17 revenue reached RM205.7 million (+12.4% QoQ, +38.9% YoY), driven by an uptick in demand for the company’s premium healthcare and cleanroom gloves.

- 1QFY17 gross profit was at RM51.8 million (25.2% gross margin), increasing 7.5% QoQ and 20.1% YoY. Despite a spike in raw material prices which impacted gross margin, the company’s tactical stockpiling of raw materials to tide over the price hike and streamlining of other operating expenses yielded 1QFY17 PAT of RM33.6 million (+23.7% YoY).

- Riverstone saw growth from both the healthcare and cleanroom glove segments in the quarter. Specifically, management’s efforts to tap new markets for cleanroom gloves have borne fruit as the company gained traction among the non-HDD sectors (namely mobile, tablet, and LCD manufacturing industries). For more details click here.

Management Outlook and Highlights

- Riverstone continues to be in expansion mode driven by growth in the Healthcare glove segment and supported by its leadership in the cleanroom glove segment.

- Net cash flows from operating activities in 1QFY17 was at RM40.4 million (vs. RM13.3 million a year ago) despite significant surge in inventories. The company also has a positive net cash position of RM122.7 million as of 31 March 2017.

- Company is currently on track for the fourth phase of its expansion plan, which will bring total production capacity to 7.2 billion pieces per annum by end 2017. Management will also continue to increase its production capacity in 2018 and 2019, reaching 10.0 billion total annual production capacity.

- While the company continues to be on an upward growth trajectory, management remains mindful of operational challenges including competition, unfavourable movements in raw material prices and foreign exchange rates. Management remains committed to employ prudent cost controls.

To read the SGX

kopi-C profile of Riverstone Holdings Executive Chairman & CEO Mr. Wong Teek Son, click

here.

UG Healthcare Corporation

Leading manufacturer of natural latex and nitrile examination gloves with a global distribution network.

Recent Earnings Release

- 3QFY17 revenue was at S$17.6 million (+16.8% YoY) which was mainly driven by increasing volume of gloves produced and sold.

- 3QFY17 gross profit was at S$3.3 million, declining 2.1% YoY while gross margin was at 18.7% (vs. 22.3% a year ago). This was mainly due to the significant increase in natural latex and nitrile raw material prices. Net profit to owners of the company was at S$0.95 million, declining 43.5% YoY. Click here for more.

Management Outlook and Highlights

- Management highlighted the volatile global macroeconomic environment, fluctuations in prices of natural latex and nitrile, as well as currencies as constant challenges for the company.

- The company will continue to drive efforts in cultivating own brand of gloves and marketing them directly to customers through their own distribution companies globally.

- Management believes the company’s expansion plan to increase production capacity (to cope with expected increase in demand) is on track to achieve the targeted annual production capacity of 2.4 billion gloves by close of FY ending 30 June 2017.

Source: Bloomberg (data as of 19 June 2017)

SGX My Gateway

SGX’s investor education portal with market, product and investment information and events. Sign up now at

sgx.com/mygateway to receive our investment updates and economic calendar.

This document is not intended for distribution to, or for use by or to be acted on by any person or entity located in any jurisdiction where such distribution, use or action would be contrary to applicable laws or regulations or would subject SGX to any registration or licensing requirement. This document is not an offer or solicitation to buy or sell, nor financial advice or recommendation for any investment product. This document has been published for general circulation only. It does not address the specific investment objectives, financial situation or particular needs of any person. Advice should be sought from a financial adviser regarding the suitability of any investment product before investing or adopting any investment strategies. Investment products are subject to significant investment risks, including the possible loss of the principal amount invested. Past performance of investment products is not indicative of their future performance. While SGX and its affiliates have taken reasonable care to ensure the accuracy and completeness of the information provided, they will not be liable for any loss or damage of any kind (whether direct, indirect or consequential losses or other economic loss of any kind) suffered due to any omission, error, inaccuracy, incompleteness, or otherwise, any reliance on such information. Neither SGX nor any of its affiliates shall be liable for the content of information provided by third parties. SGX and its affiliates may deal in investment products in the usual course of their business, and may be on the opposite side of any trades. SGX is an exempt financial adviser under the Financial Advisers Act (Cap. 110) of Singapore. The information in this document is subject to change without notice.