I’ve spent the past several weeks since I’m back, trying to figure out the various methodologies, and what is the most commonly used (amongst professional money managers, that is) ways to track returns.

Yes, it sounds trivial, but I’ve been taking it really seriously. I’d explain why later.

As with the bulk of my DD done these days, I’m kinda lazy to type out my thought processes and findings, BUT I’d share my thoughts really briefly.

Basically, I’ve come to realized that the Time Weighted Returns (TWR) and the Money Weighted Returns (MWR) can be drastically different for the same portfolio. Interactive Brokers calculates it automatically for me, and that’s how I realized it.

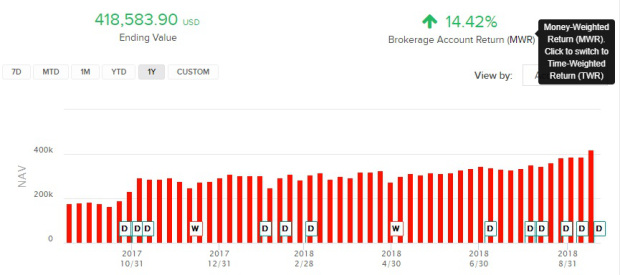

Check this out:

VS

Both these sets of returns are taken at the same time.

My global portfolio shows an annualized MWR of 14.42%, but only an annualized TWR of 10.73%.

So, which one ......