If you have a sum of money in your CPF Ordinary Account (OA), is it better to pay a greater down-payment or to take a larger loan and delay repaying your CPF Ordinary Account?

A reader of mine asked me this question and my answer to him is that based on my past research (you can read Should we repay more of our 2.6% HDB loan to save 0.1%?) it should be better to drag out the loan.

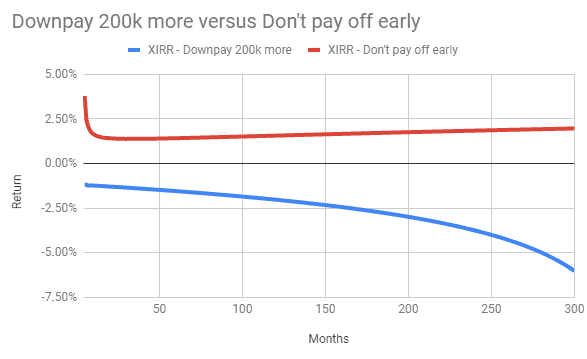

I think the general idea is that if you have more lump-sum in your CPF OA as early as possible, it allows your CPF OA to compound over time. But there are a lot of things I cannot explain why this is the case.

The question today is more clear cut because instead of choosing to consistently repay $XXX a month more towards your mortgage, we are deciding whether or not to contribute more money to downpayment or not to....