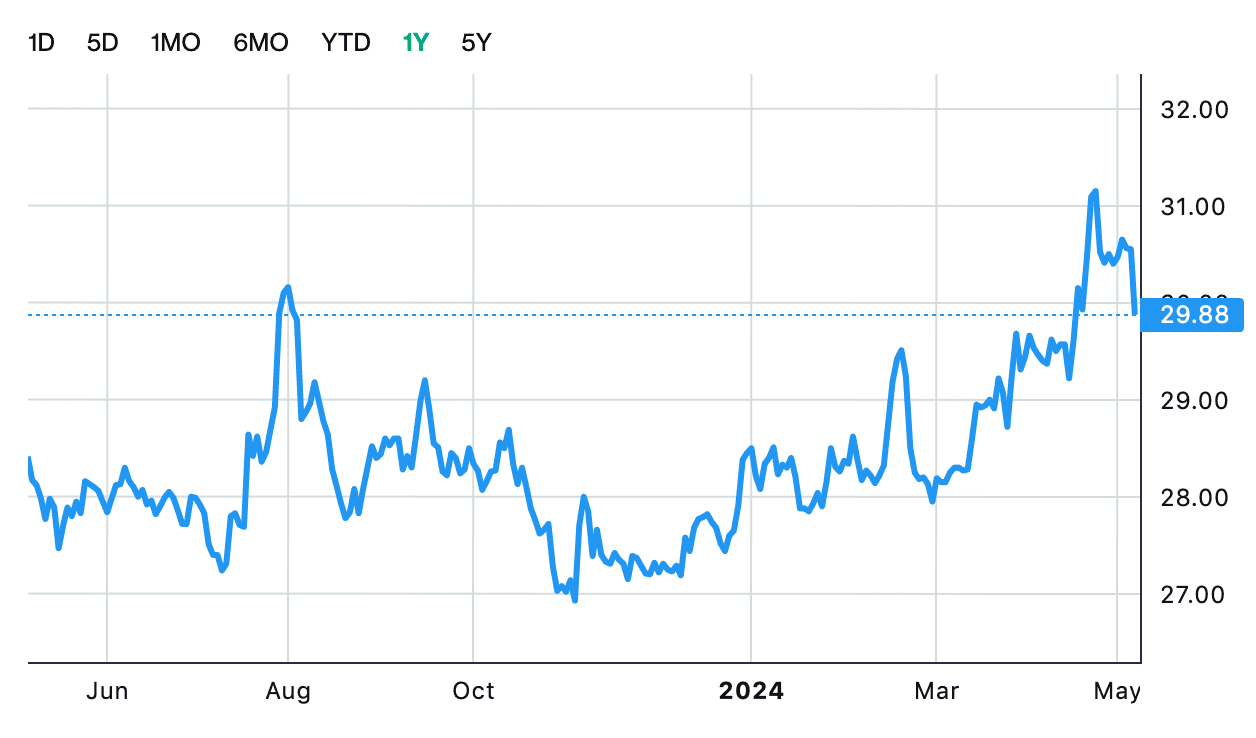

A short article with not too much detail. The two good things: IOT segment has grown tremendously at 30% CAGR over the last 3 years making up over 80% of revenue to date. Plenty of cornerstone investors including JPM Asset management.

———— The not-so good things: Track record of management is disappointing - Company previously was listed at $1.00 and delisted at S$0.42. Company interests in business outside electronics is odd - purchasing of Kay Lee Roast Meat by the parent group seemed like a strange detour from electronics focus.

A deep dive into the company found the following:

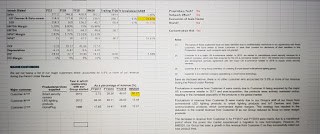

LED segment is falling significantly over the years making up about 15% of revenue now

Annualized revenue for FY20 likely fell y-o-y meaning that while some parts of the company flourished in 2020, some didn't, that is not good for a manufacturing company (supposedly less...